One of the oddest and most mysterious relationships that emerged out of the collapse of FTX last year was Alameda Research’s unusual relationship with Farmington State Bank, one of the smallest, rural banks in the United States that came under the control of Jean Chalopin in 2020. Chalopin is best known as the chairman of Deltec, one of the main banks for Alameda Research – FTX’s trading arm that played a central role in its collapse — and still one of the main banks for the largest fiat-backed stablecoin, Tether (USDT). Chalopin had acquired control over Farmington via FBH Corp., where Chalopin was listed as executive officer. Interestingly, Noah Perlman, a former DOJ and DEA official who is now Chief Compliance Officer at Binance and the son of Jeffrey Epstein associate and musician Itzhak Perlman, was also listed as a director of FBH Corp and has never publicly explained his connection with this Chalopin-controlled entity.

As Unlimited Hangout reported last December, soon after its acquisition by Chalopin’s FBH Corp., Farmington “pivoted to deal with cryptocurrency and international payments” after decades upon decades of serving as a single branch community bank in rural Washington. Soon after its pivot into the crypto space, Farmington struggled to move money and sought approval to become part of the Federal Reserve system. It also changed its name from Farmington State Bank to Moonstone Bank. The approval of Farmington by the Federal Reserve has been deemed highly unusual and as having “glossed over Moonstone’s for-profit foreign interests.” Late last December, Eric Kollig, spokesman for the Federal Reserve, told reporters that he could not comment “about the process that federal regulators undertook to approve Chalopin’s purchase of the charter of Farmington State Bank in 2020.”

Just days after Farmington formally changed its name to Moonstone in early March 2022, FTX-affiliated Alameda Research poured $11.5 million into the bank, which was – at the time – more than twice its entire net worth. Moonstone’s Chief Digital Officer, Jean Chalopin’s son Janvier, later stated that the funding from Alameda Research had been “seed funding … to execute our new plan of being a tech-focused bank.”

Upon Alameda’s taking a stake in the bank, Jean Chalopin stated that this move “signifies the recognition, by one of the world’s most innovative financial leaders, of the value of what we are aiming to achieve. This marks a new step into building the future of banking.” Outlets like Protos have noted how unusual it is that a Bahamas-based company like FTX was “able to purchase a stake in a federally approved bank” without attracting the attention of regulators.Washington State regulators have stated that they were “aware” of Alameda’s investment in Farmington/Moonstone and defended their decision not to intervene or take further regulatory action.

Notably, the influx of new money into the remodeled Farmington was not exclusive to FTX/Alameda. A New York Times article on the matter noted that Farmington/Moonstone’s deposits – which had hovered around $10 million for many decades – quickly surged to $84 million, with $71 million coming from only four new accounts during this same relatively short period in 2022.

As Unlimited Hangout previously noted, the same day the Alameda investment was announced, Moonstone installed Ronald Oliveira as CEO. Oliviera had previously worked for the fintech company Revolut, a “leading digital alternative bank” financed by Jeffrey Epstein associate Nicole Junkermann. Roughly two months later, the bank hired Joseph Vincent as its legal counsel. Immediately prior to joining Farmington/Moonstone, Vincent had served as the general counsel for Washington State’s Department of Financial Institutions and its director of legal and regulatory affairs for 18 years.

Shortly before FTX’s collapse, which put Farmington/Moonstone under heavy scrutiny, Farmington/Moonstone partnered with a relatively unknown company called Fluent Finance. Fluent Finance, both then and now, has evaded scrutiny from the media aside from Unlimited Hangout’s investigation into Farmington, published last December. However, since FTX’s unraveling and the shuttering of Farmington/Moonstone in the months that followed, Fluent Finance has been quite busy, developing significant government partnerships in the Middle East and looking to become a central part of the coming Central Bank Digital Currency (CBDC) paradigm for both West and East.

A likely reason behind the lack of media interest in Fluent Finance and their apparent success after the FTX scandal is the fact that Fluent, from its earliest days, has been operating as an apparent front for some of the most powerful commercial banks in the world and building out “trusted” digital infrastructure for the economy to come. This investigation, an examination of Fluent’s past and its current trajectory, may help elucidate the true motives behind the efforts of Chalopin, Bankman-Fried and others to turn the tiny Farmington State Bank into “Moonstone.”

Fluent Finance’s Deep and Early Connections to Wall Street Banks

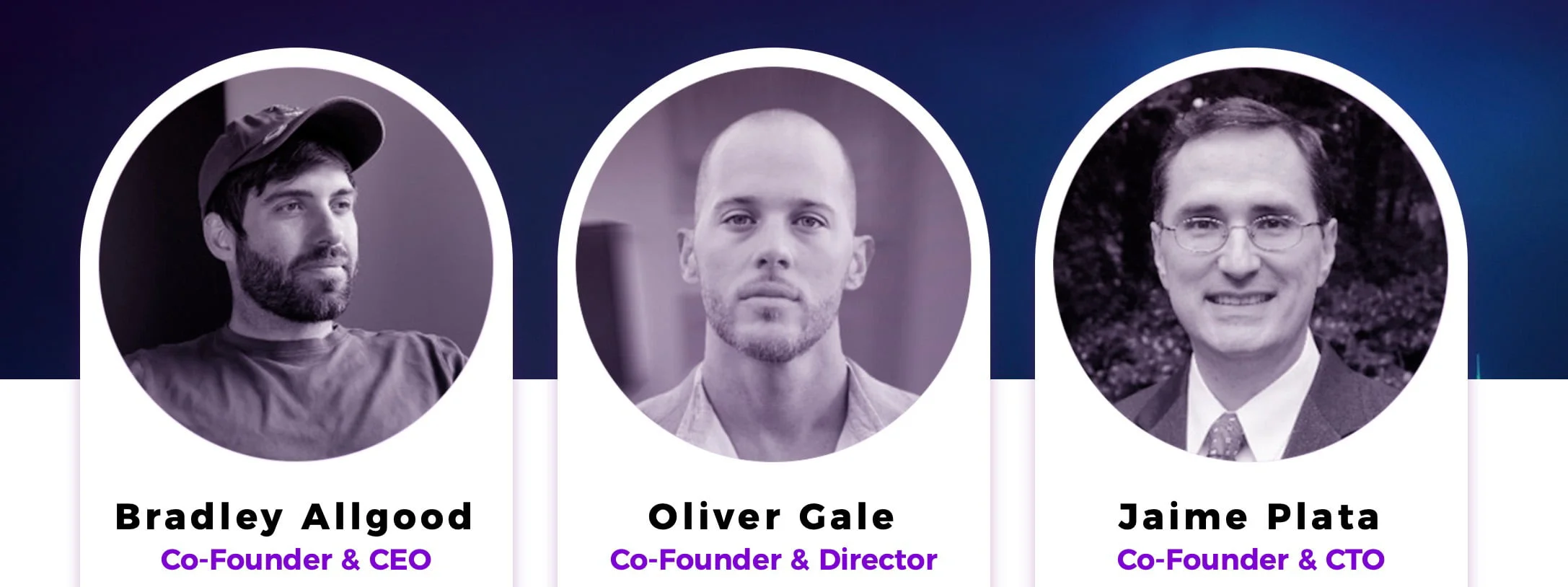

Fluent Finance was created in 2020 and was co-founded by Bradley Allgood, Oliver Gale and Jaime Plata. Allgood began his career with the US Army and later went on to serve in NATO’s Governmental Operations division with an apparent focus on NATO activity in Afghanistan. After leaving NATO, Allgood “immediately jumped” into economic development, specifically the creation and expansion of Special Economic Zones (SEZs), specifically one partnered with the Catawba Indian Reservation in South Carolina. That SEZ, officially named the Catawba Digital Economic Zone, was co-founded by Allgood in 2019 and he still serves as its head of Commercial Banking.

Sitting on just two acres of land, the zone aims to “become the worldwide registration hub for crypto companies” as well as to “take a huge chunk out of Delaware’s market for company registration or even to replace it as the gold standard.” The zone is backed by a venture capital firm tied to Bradley Tusk, the former Deputy Governor of Illinois under disgraced former Governor Rod Blagojevich and the former campaign manager for billionaire Mike Bloomberg. In addition, Tusk’s companies count Google, the Rockefeller Foundation and Ripple (XRP) among their clients. Tusk’s different VC firms have invested in Coinbase and Circle, the issuer of the USDC stablecoin, and Uber as well as the economic zone co-founded by Allgood.

Shortly after leaving the military, Allgood also worked on the early development of digital transformation of governments, digital identities, people and property registries and the tokenization of carbon credits and commodities. Later motivated by “the sheer number of unbanked and underbanked in the world”, Allgood hosted roundtables around the world with central bank “regulators, tier one institutions, innovators, [and] technology providers” and decided he could act as “a good connector” for the different actors in his growing network.

Allgood claims to have spoken to a few “really senior” banking executives at HSBC, Citi and Barclays and to have educated “them on new innovative technologies for custody [and] better digital identity.” After “building a team” of these “senior bankers from tier one financial institutions,” Allgood and his team “went out into the market and started servicing the [cryptocurrency] space and helping innovative companies find homes and large core banking systems and tier one financial institutions.” While working with these various titans of finance and guiding their views on the future of banking, Allgood met his co-founders of Fluent Finance: Oliver Gale and Jaime Plata.

Oliver Gale is one of the co-founders of Central Bank Digital Currencies (CBDCs), having pioneered the first CBDC project in the Eastern Caribbean and, per Allgood, Gale “went on to do them in Nigeria” and helped create the highly controversial e-Naira. Gale notably describes himself as the inventor of CBDCs and has previously collaborated with the UN, MIT and the IMF. Jaime Plata, Fluent’s other co-founder, “did the core banking systems of the Eastern Caribbean Central Bank during the first CBDC [launch].” Aside from Gale and Plata, Allgood has revealed that other top Fluent Finance executives, who are not listed on the company’s website, hail from the Wall Street titan Citi – with the company’s CFO being “the CFO of Citi of all of Latin America” and its COO being “one of the senior, most senior, managing directors from Citi.” He has also stated that other important employees of Fluent include the former chief innovation officer of General Electric as well as “an early board member at [the now collapsed crypto exchange] Celsius [that] helped them get to market.”

Fluent Finance was initially founded with two main and interrelated products: the Fluent Protocol and the US+ stablecoin. Fluent has described the Fluent Protocol as “a financial network that seamlessly bridges traditional finance and digital assets,” while US+ is a “bank-led”, US dollar-pegged stablecoin “built on principles” and designed to be “forward-compatible with CBDC initiatives.” Fluent asserts that US+ resolves “the inherent flaws of web3-native stablecoins” by having US+ be operated by a network of banks partnered with Fluent Finance. Fluent has not made the identities of these banks available to the public.

“When we examined stablecoins, we knew that the lack of institutional uptake of the technology was due to risk,” explained Allgood. “With that in mind, when we approached the design of US+, we did so in terms of de-risking. We knew we needed to provide real-time and transparent reserves monitoring.” Fluent’s answer to providing the reserve metrics needed to tap into the heavily regulated traditional finance market emerged through its partnership with Chainlink, first announced in September 2022.

Chainlink is a blockchain oracle network, meaning it connects blockchains to external systems. It was launched in 2017 on the Ethereum blockchain and later registered in the Cayman Islands as SmartContract Chainlink Limited SEZC in March 2019. In December 2021, the former Google CEO Eric Schmidt, who has unprecedented control over the Biden administration’s technology policies, joined Chainlink Labs as a strategic advisor. At the time, Schmidt commented that “it has become clear that one of blockchain’s greatest advantages — a lack of connection to the world outside itself — is also its biggest challenge.”

Fluent’s partnership with Chainlink dealt with regulatory necessities by providing a reliable way for the Fluent Protocol to access real-time, off-chain data from external sources. Fluent’s goal was/is to provide proof of the size, performance, and risk of its asset reserves in order to meet its stablecoin protocol liquidity requirements. Reliable confirmation and publishing of the state of these reserves was seen as crucial by Allgood and others at Fluent in order to manufacture trust from both retail users and membership banks.

Fluent is far from the only partner of Chainlink working on providing trusted stablecoin reserve architecture. Among them is Paxos, the former issuer of Binance’s BUSD and their own PAX, and who recently began providing infrastructure for PayPal’s PYUSD stablecoin. Paxos relied on Chainlink to provide on-chain Proof of Reserve Data Feeds for Paxos’ assets, ensuring verification that PAX tokens are 1:1 backed by US Dollars. This was taken a step further with their gold-backed PAXG tokens, in which Chainlink claimed to be able to provide verification of off-chain, physical gold bars held in Paxos’ custody.

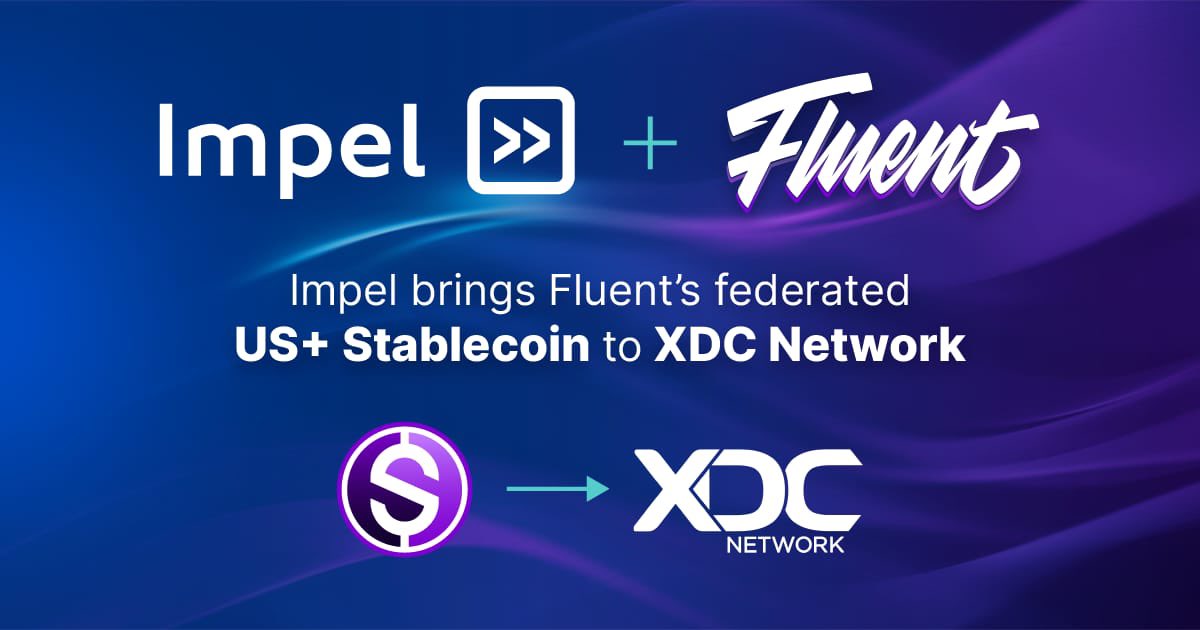

Another Chainlink partner is the XinFin Network, also known as the XDC network, which uses Chainlink’s Price Reference Data framework to introduce price feeds for major national currencies such as the Hong Kong Dollar, the Singaporean Dollar, and the United Arab Emirates Dirham. In October 2022, Fluent Finance announced a partnership with Impel to bring its US+ stablecoin to the XDC network. Impel itself is a startup birthed out of XinFin Fintech led by CEO and founder Troy S. Wood. The company boasts a team of advisors including XDC Network co-founders Ritesh Kakkad and Atul Khekade, in addition to long time SWIFT employee André Casterman.

In March 2021, XinFin leveraged the DASL Crypto Bridge designed by LAB577 to bring their XDC token to R3’s Corda blockchain. R3 began as a consortium of banks and is not only closely connected to Fluent Finance, but, as will be discussed shortly, is also a major driver of CBDC and stablecoin development globally. Before this XDC-Corda bridge was created, there was no liquidity or token of value on the R3 Corda Network. This bridge opened up the opportunity for traditional financial institutions, such as those that fund R3, to interact with cryptocurrency indirectly without having to operate on under-regulated public networks that could land them in hot water with regulators. It also gives access to those already utilizing Ethereum-based tokens (i.e. ERC20 or ERC721) to the business networks and financial institutions on the Corda network.

XDC co-founder and Impel advisor Atul Khekade remarked that the both government regulators and commercial banks had settled on XDC and Corda as the means through which many major banks would access blockchain technologies:

“Regulatory agencies and financial institutions have selected both Corda and the XDC Network as suitable platforms to engage with blockchain technology […] They did not just randomly throw a dart at a board.”

Fluent Meets Moonstone

In late October 2022, Fluent Finance, now deeply ensconced in the Web3 ambitions of major commercial banks, announced its partnership with Farmington/Moonstone. In a press release on the partnership, Fluent wrote that “Moonstone will be a custody partner in Fluent’s growing network of banks, with plans to expand into a full-node member soon,” which would “allow Fluent and Moonstone to connect the traditional financial system to the emerging Web3 economy.”

At the time the partnership was announced, Fluent’s CEO Bradley Allgood stated the following:

“Moonstone Bank is now a key player in Fluent’s financial ecosystem and will serve as an initial custodian partner. Fluent plans to eventually bring Moonstone Bank on as a full-node partner, which will allow the bank to mint and burn US+. Collaborating with Moonstone is incredibly exciting and will help Fluent bring a safe and secure stablecoin to market while allowing for instant payments along with lower fees. It will also clearly demonstrate the benefits that stablecoins can bring to the banking sector, businesses, and everyday end users alike.”

Notably, this was – and remains – the only Fluent Finance press release to name a member of Fluent’s consortium that supports its “bank-led” stablecoin, US+. In addition, given Allgood’s statements on the partnership, he clearly felt that partnering with Moonstone was a critical part of bringing US+ to market.

However, with the collapse of FTX that November, Farmington/Moonstone came under heavy scrutiny, even attracting the attention of U.S. Senators who cited Farmington/Moonstone’s relationship with FTX as reason to launch federal investigations into the relationships between banks and cryptocurrency firms. The many unanswered questions about Alameda’s relationship with Farmington/Moonstone, Chalopin’s involvement and potential connections to Deltec and Tether as well as the apparent negligence of regulators caused major reputational and trust issues for Farmington/Moonstone.

A few months after the FTX collapse, in January 2023, Farmington announced it would drop the Moonstone name and return to its “original mission as a community bank” and would discontinue “its pursuit of an innovation-driven business model to develop banking services for industries such as crypto assets or hemp/cannabis.” Just a few days after that announcement, federal prosecutors seized $50 million from Farmington/Moonstone, which they alleged had been deposited as “part of FTX founder Sam Bankman-Fried’s wide-ranging scheme to defraud investors through his massive cryptocurrency exchange business.” That sum, significantly more than what Alameda Research had initially invested, was more than half of the bank’s total assets based on the most recent FDIC filings at the time of the seizure. The $50 million seized was all under one account under the name of “FTX Digital Markets,” per court records cited by local Washington newspapers.

Then, in May, the bank announced it would be selling its deposits and assets to the Bank of Eastern Oregon. The Federal Reserve subsequently took enforcement action against Farmington as well as its parent FBH Corp. a few months later in August. According to local newspapers, the Fed “issued a cease-and-desist order against the firms and directed them to take a number of actions as Farmington closes its business – including preserving records and not acquiring any additional brokered deposits.” The Fed asserted that Farmington had violated commitments it had made as part of the approval process which granted it access to the Federal Reserve system. However, it is unknown which commitments were allegedly violated, as the Fed has refused to come clean about its highly unusual and irregular approval of Farmington/Moonstone, even after its enforcement actions against the bank. Fluent Finance issued a statement after the Fed’s announcement and referred to Farmington for the first time as a “prior tentative” collaborator and sought to distance itself from the bank. Most recently, in November, FBH Corp., Jean Chalopin’s vehicle for acquiring and then controlling Farmington, failed to file an annual report in Washington State for 2023, meaning that it will be terminated sometime within December.

While 2023 could not have been worse for Moonstone/Farmington, Fluent Finance managed to successfully reinvent itself by partnering with the government of the United Arab Emirates (UAE) and R3, a blockchain company that focuses on accelerating digital currencies (particularly CBDCs) and is backed by some of the biggest banks in the world.

Building the Rails for CBDC settlement in the UAE

In late July, a few weeks before the Fed announced its enforcement action against Farmington/Moonstone, Fluent Finance announced that they would be opening an office in Abu Dhabi in the United Arab Emirates, an expansion explicitly backed by the UAE Ministry of Economy. According to a press release, “As part of their move into the region, Fluent Finance is getting support from the office of the Ministry of Economy, further cementing their relationship with regulators and leaders in the region to unveil innovative solutions for cross-border payments.” The UAE government was explicitly backing Fluent Finance so that the company could “advance the UAE’s trade finance and cross-border payments landscape.”

Fluent’s new UAE entity, called Fluent Economic Bridge, focuses on deposit tokens, i.e. commercial bank-issued tokens backed by deposits, with the explicit intention of connecting deposit token and CBDC systems within the UAE and, eventually, beyond. As previously mentioned, Fluent is partnered with the company R3, which is currently under contract with the UAE’s Central Bank to build out the nation’s CBDC system. Fluent Economic Bridge uses R3’s Corda DLT (distributed ledger technology) in order to “bring CBDC-compatible deposit token infrastructure for borderless payments.”

A few months later, in October, Fluent Finance – described in reports from this period as a “US-based developer of a cryptocurrency-based payment platform” – joined an UAE government program called NextGenFDI, which aims to offer a litany of incentives to foreign web3-focused companies to relocate to the country. Reports praising Fluent’s participation in the program noted that Fluent’s focus had moved to “mak[ing] cross-border trade easier” and that the company’s UAE-based Fluent Economic Bridge would be “used by importers and exporters to settle transactions through bank-issued cryptocurrencies, known as stablecoins or deposit tokens.” “I am optimistic about the possibilities of the Fluent Economic Bridge, and the potential for digital currencies to improve the efficiency and accessibility of global supply chains,” UAE Minister of State for Foreign Trade Dr. Thani Al Zeyoudi was quoted as saying.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/thenational/CVJ5VDESGRAQBP2LQATMU2F4AQ.jpg)

Fluent’s collaboration with the UAE government was notably designed to align “with the [UAE’s] Ministry of Economy’s TradeTech initiative, which, with the participation of the World Economic Forum, aims to promote the use of advanced technology tools in global supply chains, as well as the country’s comprehensive economic partnership agreement programme, which aims to achieve frictionless trade between the UAE and other economies.”

Articles on the development also stated that “by working with banks and regulators in Abu Dhabi, Fluent aims to boost the transparency of cryptocurrency with the security and regulatory structure of the traditional banking system.” Claims were made that Fluent has been piloting this program in Kenya, but Fluent’s website makes no mention of any such program and no information about any such pilot is available online at the time this article was published. This suggests that Fluent’s pilot in Kenya is operating under a different name with no overt ties to the company being publicized.

A few days later, Emirati news reported that Fluent Finance would be partnering with the UAE’s Ministry of Economy to develop “deposit token-based tech” and “stablecoin technologies.” The company stated that by “collaborating with banks and regulators[,] its platform provides the immediacy and transparency of cryptocurrency with the security and regulatory structure of the traditional banking system.” Allgood framed much of the collaboration as a key part of the UAE’s effort to “modernize” multilateral trade. He stated that “The UAE has positioned itself as a global leader for digital assets through their special economic zone initiatives, regulation foresight, and global trade expansion with strategic MoUs [memorandums of understanding],” specifically MoUs with India and China, key members of the BRICS bloc. Since these reports, even more MoUs have been signed between the UAE and BRICS countries. For instance, earlier this month, China’s central bank signed a $400 million “cooperation memorandum” with the UAE’s central bank that is specifically focused on the interchange of the countries’ respective CBDCs. As previously noted, the UAE’s coming CBDC, the digital dirham, is being developed by R3, which is closely tied to Fluent Finance.

A report in Gulf Business on Fluent’s collaborations with the UAE noted that, with respect to the MoUS, “the agreements account for more than $100bn in bilateral trade, with a focus on strengthening the use of new technologies and settlement with digital currency. Deposit tokens issued by commercial banks are poised to offer a borderless missing link to accelerate trade settlement to central bank digital currency.” In other words, it seems that Fluent is positioning itself as an accelerator for CBDCs via deposit tokens, related infrastructure and its “low counterparty risk stablecoin” US+.

R3 – Accelerating Financial Surveillance

Further evidence of Fluent’s intentions to accelerate a CBDC-deposit token paradigm can be found in Fluent Finance’s cozy relationship with R3, a self-described “leader in the digitization of financial services” that is responsible for the Corda DLT platform. As previously mentioned, R3’s backers include some of the biggest names in finance, among them several of the massive commercial banks who had an early role in the creation of Fluent Finance.

Fluent’s connection with R3 was present early on, including before its ill-fated attempt to partner with Farmington/Moonstone. For instance, Fluent’s early partnership with XDC in October 2022 was influenced by the fact that XDC was also “heavily related to R3” as well as XDC’s focus on “trade finance” according to Allgood. Notably, XDC is also very active in the UAE and was described by Emirati media as a “driving force” behind the country’s ambition to become “the successor to Silicon Valley” in articles published roughly a month before Fluent announced its partnership with the UAE’s Ministry of Economy.

In addition, Fluent’s head of engineering Will Hester, who joined the company in April 2022, previously worked as R3’s tech lead and previously as a R3 software engineer. Other Fluent employees, such as software engineer John Buckle, had also previously worked for R3. In addition, Fluent Finance’s US+ utilizes a private Corda network (Corda being a R3 product) to tokenize US+’s fiat currency (i.e. US $) reserves. Reports on Fluent’s expansion into the UAE note that the company chose to use Corda in order to “introduce CBDC-compatible deposit token infrastructure for borderless payments.”

While Fluent has been relatively quiet about its commercial banking partners, what Allgood has revealed is an apparent association between the early days of the company with HSBC, Citi and Barclays, suggesting that these banks could be among the members of its banking consortium backing its US+ stablecoin. R3, which notably began as a consortium of commercial banks, is backed by major banks including HSBC, Citi and Barclays as well as other top names in finance including BNY Mellon (which now holds the bulk of the reserves for the USDC dollar-pegged stablecoin after the banking crisis earlier this year), Deutsche Bank and Wells Fargo. R3’s relationship with Wells Fargo is particularly notable as the company’s Corda platform is playing a critical role in Wells Fargo’s pilot of a dollar-pegged stablecoin that will be used “initially for internal settlement across the company’s business.” The Wells Fargo dollar-pegged stablecoin on Corda is being pitched for essentially the same use cases as Fluent’s US+.

Though R3 has considerable ties to a coming digital dollar, through Wells Fargo, Fluent Finance and others, they are also a key player in a number of CBDC projects globally. As previously mentioned, in April of this year, the UAE announced that it had selected R3 to begin implementing its CBDC strategy. The company, which describes itself as having been “at the forefront of CBDC innovation since 2016,” is also involved with CBDC development in France, Kazakhstan, South Africa, Australia, Malaysia, Switzerland, Singapore, and Sweden and is partnered directly with the central banks of those countries. R3 was also involved in Italy’s Project Leonidas, a wholesale CBDC trial between Italy’s central bank and the Italian Banking Association. R3 was even named 2023’s CBDC partner of the year by the publication Central Banking.

However, R3 is focused on much more than CBDCs, as evidenced by their Digital Currency Accelerator (DCA), which offers “an end-to-end solution that enables central banks, commercial banks, and monetary authorities to issues, manage, transact, and redeem CBDCs and privately-issued digital currencies.” In other words, R3’s DCA facilitates the creation of CBDCs for central banks and deposit tokens and stablecoins for commercial banks, all of which would likely be inter-operable with other currencies on R3’s Corda network. The central bank component of the DCA, the CBDC accelerator, was designed specifically to meet CBDC specifications laid out by the Bank of International Settlements (BIS). R3’s CBDC accelerator, as well as what it offers for deposit tokens, allows the issuer to “define and configure a delegated programmability framework,” which is important given that programmability is one of the most controversial components of CBDCs.

One key partnership highlighting R3’s role in accelerating commercial banks’ forays into the digital currency era was forged in August 2022, when R3, along with The Depository Trust & Clearing Corporation (DTCC) –– a prominent post-trade market service provider in the global financial services industry — announced the successful launch of its Project Ion platform. This private and permissioned Distributed Ledger Technology (DLT) platform was developed in collaboration with key industry players (most of whom directly back R3) and technology providers such as BNY Mellon, Charles Schwab, Citadel Securities, Citi, Credit Suisse, Fidelity, Goldman Sachs, J.P. Morgan, Robinhood Securities, and the State Street Corporation, among others. In 2011 alone, DTCC facilitated the settlement of the majority of securities transactions within the United States and processed nearly $1.7 quadrillion in transactions, solidifying its position as the world’s foremost financial value processor.

In order to best take advantage of the coming issuance of trillions of dollars in highly regulated stablecoins, R3 purchased stablecoin issuer Ivno in October 2021. This acquisition came only 6 months after the completion of a collateral tokenization trial Ivno had held with 18 partnered banks including Egypt’s CIB, Singapore’s DBS, Brazil’s Itaú Unibanco, National Bank of Canada, Natixis, Austria’s Raiffeisen Bank International and US Bank as well as three unnamed securities exchanges.

Invo was far from the only prospective stablecoin issuer that have partnered with R3. For instance, in September 2019, Fnality and Finteum both joined forces to leverage their Utility Settlement Coin (USC) on the Corda blockchain. Fnality, headed by CEO Rhomaios Ram, the former Global Head of Product Management for Transaction Banking at Deutsche Bank, identifies as a wholesale payments firm, and boasts institutional shareholders such as Goldman Sachs, Barclays, BNY Mellon, CIBC, Commerzbank, DTCC, Euroclear, and ING, among others. In December 2023, Fnality, along with Lloyds Banking Group, Santander and UBS, executed the first ever transaction settlement of digital central bank funds with balances of sterling using an “omnibus account” at the Bank of England. The weight of the moment was not lost on Hyder Jaffrey, Managing Director at UBS: “The creation of a new systemically important global payment system is a once in a generation event.”

With the DTCC’s experience in settling the lion’s share of dollar-denominated securities, and with Fnality and Ivno’s collaborations with some of the largest players in the international banking system, R3 have quietly positioned themselves as suppliers of potentially essential infrastructure within the imminent global system of interoperable CBDCs and their commercial bank equivalents.

R3 partner Fluent Finance, and more specifically its UAE-based Fluent Economic Bridge, is seeking to serve as the connective tissue between the deposit tokens and stablecoins to be issued by commercial banks both in the UAE, as well as abroad, and CBDCs by ensuring their compatibility. Indeed, Fluent’s website – in both the past and present – has promoted its products’ “CBDC bank compatibility.” Given Fluent’s long-standing collaboration and affiliation with R3 and the banks behind it, Fluent Economic Bridge and its stablecoin protocol have likely been built with CBDCs running on R3’s Corda in mind.

In addition, just as R3 is developing CBDCs and other digital currencies far beyond the UAE, Fluent is also looking to expand its “economic bridge” and US+ far beyond the Emirates. In an interview Allgood gave to R3 on January 2023, he stated that Fluent has been in talks with the UAE government to issue a US+ equivalent but for their local currency, the dirham (i.e. a bank-issued dirham stablecoin that would be interoperable with its R3-developed CBDC). He also claimed to be far along in developing a US+ equivalent for the Mexican peso.

In addition, in the same interview, Allgood revealed that Fluent is “looking to do a US dollar stablecoin but with local banking in Africa” and is in talks with multiple banks across 36 different African countries in pursuit of that particular project. Allgood, while busy championing and building an interoperable network of CBDCs across the globe, has begun to turn Fluent’s attention beyond just US+ and towards the dollar system itself.

Building the Digital Dollar: The Synthetic Deposit Token

The US, despite the launch of CBDC pilots in China, Japan, Russia, India, Israel, Saudi Arabia, the UAE, and elsewhere, has yet to formally launch any sort of government-issued digital dollar. In a June 2023 white paper titled “Central Bank Digital Currency Global Interoperability Principles”, the World Economic Forum reflected on the serious push by governments around the world to explore CBDC issuance. The paper makes mention of “over 100 countries actively engaged in CBDC research and development”, while quoting the managing director of the International Monetary Fund, Kristalina Georgieva, making the distinction that “there is no universal case for CBDCs because each economy is different”. It seems that the US has plans to be “different” from most countries. For instance, in November 2022, two days before FTX filed for bankruptcy, Coinbase CEO Brian Armstrong was a guest on the Circle CEO Jeremy Allaire’s podcast, and stated that “every major government pretty much is going to want to have a CBDC”, while delineating the path for the US would likely be different from the rest of the world. “I think in the US’s case, it is going to end up using USDC [the dollar-pegged stablecoin issued by Circle] as sort of like a de facto CBDC.”

In the WEF’s white paper, two US efforts related to CBDCs are mentioned: Project Hamilton, the Boston Fed’s 2020 collaboration with the Massachusetts Institute of Technology’s (MIT) Digital Currency Initiative; and the 2022 report by The New York Fed titled Project Cedar. The former, Project Hamilton, focused mostly on payment throughput of a retail-facing digital currency, while the latter, Cedar, was an experiment on a deposit token to be exchanged by banks during wholesale settlement. The delineation between Project Hamilton and Project Cedar is nearly identical to the fork in the road currently facing the founding fathers of the coming digital Federal Reserve.

In a February 2022 analysis, Gerard DiPippo – an 11 year veteran of the US intelligence community (specifically the CIA) who has long been focused on economic issues in the Global South – stated that:

“Dollar stablecoins have at least one major advantage over a potential U.S. CBDC: they already exist. Even if Congress were to decide the Fed should create a CBDC, the process of development, experimentation, and deployment would probably take at least a few years.”

In that same analysis, published by the National Security State-adjacent Center for Strategic and International Studies (CSIS), DiPippo added that: “The United States should not delay in establishing a regulatory framework to enable safe but speedy development of dollar stablecoins to gain a first-mover advantage in related payments and technologies.”

Indeed, just as DiPippo noted, the digital dollar is already here. In fact, it has been here for a long time. A Fall 2021 piece from Harvard Business Review made the claim that “over 97% of the money in circulation today is from checking deposits – dollars deposited online and converted into a string of digital code by a commercial bank.” But while the vast majority of dollar circulation may have been reduced to 1’s and 0’s on some private bank’s spreadsheet over the last few decades, the assets that actually uphold the US dollar system — US Treasuries — have evolved to the digital age a bit slower. While programs like TreasuryDirect do exist, in which users can set up an account online and purchase securities directly issued by the US Department of Treasury, the actual interbank securities clearing network had remained relatively antiquated until the launching of FedNow this past summer.

FedNow, on first glance, seems innocuous enough – a new communications tool for Federal Reserve-partnered banks to exchange securities. But, on second glance, its necessity in the 21st century implementation of dollar hegemony becomes clear. The settlement and exchange of Treasuries, the asset that actually backs the digital dollars created from checking deposits by private capital creators, has now become further regulated, centralized, and controlled.

A reverse repo, or a reverse repurchase agreement, is the preferred method for banks to seek yield by temporarily loaning securities, specifically Treasuries, for cash due to the fact that each party physically exchanges the assets, with an agreement to repurchase the securities the next day with an added service fee. Banks much prefer to do this as opposed to a more traditional loan structure due to the mitigated liability risk that comes downstream of physically holding on to the collateral in the agreement. Say a cash-strapped bank has recently secured a loan to meet current liquidity needs, but before they can repay the loan, the culmination of financial woes causes the bank to declare bankruptcy and ultimately be seized by authorities. The lending bank now not only loses out on its service payments, but also the entire liability of the loan principal. If they had agreed to a reverse repo exchange, while the lender would still lose out on collecting their fees, they would at least retain the rights to the exchanged Treasuries currently within their custody.

The US banking system makes a lot of money by buying US Treasuries and using them to create dollars. The US Department of Treasury also benefits as it is able to service the budget of the US government by selling its debt to the US banking system. Neither of these entities want to muck up their racket: The US government doesn’t want to be directly responsible for managing retail account balances for citizens (as would be the case with a direct-issued dollar CBDC), and the biggest banks certainly don’t want to lose their effective monopoly of private capital creation by letting some outsider fintech company secure the contract for directly issuing digital dollars for the government. FedNow is strictly a wholesale product. In fact, it isn’t really a product at all ––there is no token and it only aims to allow regulators to more closely surveil the exchange of Treasuries.

The purchasing of Treasuries, however, is rapidly shifting towards an entirely new customer class: stablecoin issuers. Much like how a private-sector bank would purchase government-issued securities to back the issuance of dollars in a retail checking account, stablecoin issuers such as Tether (USDT) or Circle (USDC) have become net-buyers of short-term Treasuries referred to as T-bills. Tether CEO Paolo Ardoino tweeted in September 2023 that “Tether reached $72.5 billion exposure in US T-bills, being [a] top 22 buyer globally, above the United Arab Emirates, Mexico, Australia and Spain.” Just three months later, in December 2023, Tether’s Treasury holdings were over $90 billion. For reference, the largest single holder of US Treasuries is Japan with just over $1 trillion held –– Tether alone already commands nearly a tenth of their balance sheet. In our current high interest rate environment, the yield from these short duration securities can be substantial, leading to large revenue streams for not only these stablecoin issuers, but the companies and banks that custody their assets.

Tether’s substantial Treasury holdings are distributed among three main custodians: Charles Schwab, Fidelity and Cantor Fitzgerald. Cantor Fitzgerald is perhaps most famous for having its flagship office destroyed during the events of 9/11, but it continues today as one of the 24 primary dealers authorized to trade US government securities with the Federal Reserve Bank of New York. Earlier this month, Howard Lutnick, the CEO of Cantor Fitzgerald, made an appearance on CNBC Money Movers Podcast in which he stated “I’m a big fan of this stablecoin called Tether…I hold their treasuries. So I keep their treasuries, and they have a lot of treasuries.” He further stated his affinity for the company by making reference to Tether’s recent trend of blacklisting of retail addresses flagged by the US Department of Justice. “With Tether, you can call Tether, and they’ll freeze it.”

Just this October, Tether froze 32 wallets for alleged links to terrorism in Ukraine and Israel. In November, $225 million was frozen after a DOJ investigation alleged that the wallets containing these funds were linked to a human trafficking syndicate. This month alone, over 40 wallets found on the Office of Foreign Assets Control’s (OFAC) Specially Designated Nationals (SDN) List have been frozen. Ardoino explained these actions by stating that “by executing voluntary wallet address freezing of new additions to the SDN List and freezing previously added addresses, we will be able to further strengthen the positive usage of stablecoin technology and promote a safer stablecoin ecosystem for all users.” Just a few days ago, Ardoino claimed that Tether has frozen around $435 million in USDT for the US DOJ, FBI and Secret Service. He also explained why Tether has been so eager to help the US authorities freeze funds – Tether is seeking to become a “world class partner” to the US to “expand dollar hegemony globally.”

The stablecoin ecosystem, where US dollar-pegged stablecoins dominate, has become increasingly intertwined with the greater US dollar system and – by extension – the US government. The DOJ has the retail-facing Tether on a leash after pursuing the companies behind it for years and now Tether blacklists accounts whenever US authorities demand. The Treasury benefits from the mass purchasing of Treasuries by stablecoin issuers, with each purchase further servicing the federal government’s debt. The private sector brokers and custodians that hold these Treasuries for the stablecoin issuers benefit from the essentially risk-free yield. And the dollar itself furthers its effort to globalize at high velocity in the form of USDT, helping to ensure it remains the global currency hegemon.

In effect, Treasuries are being bought hand over fist, and dollars are being spent en masse. Much like the discrepancy between Bitcoin’s UTXO or coins model and Ethereum’s account balance model, Treasuries and dollars behave exceptionally differently in economic terms. A government could never directly issue what is known as M0 –– base money –– to retail accounts, and thus a CBDC could never serve as anything but M1 — a programmable checking account that relies on trust in a financial service provider to be exchanged. Perhaps a directly-issued US dollar-denominated CBDC is a red-herring. Just ask the Fed.

For instance, Federal Reserve Vice Chair for Supervision Michael Barr stated this past November that “There’s obviously a lot of innovation happening in the private sector,” while later implying that the Federal Reserve has a “very strong interest” in regulating, approving and supervising US dollar-pegged stablecoin issuers. Deputy Secretary of the Treasury Wally Adeyemo recently lobbied Congress on behalf of the US Treasury to extend the regulatory powers over dollar-denominated stablecoins beyond US companies and even US citizens. “Legislation could explicitly authorize OFAC to exercise extraterritorial jurisdiction over transactions in stablecoins pegged to the USD (or other dollar-denominated transactions) as they generally would over USD transactions,” the proposal suggested, even for transactions that “involve no U.S. touchpoints.”

Last month, the Atlantic Council also wrote of “the current [Federal Reserve] policy trajectory favoring private stablecoin issuance rather than official CBDC issuance,” making note of an August 8 regulation letter stating that “the Federal Reserve formally shifted its stance to promote stablecoin issuance by banks.”

Over a year before Barr’s statements or the Atlantic Council’s post, Bruno Sultanum, an economist in the Research Department at the Federal Reserve Bank of Richmond wrote in a July 2022 brief that “privately issued stablecoins could be equivalent to CBDCs” and that “there may be a pathway to create an effective ‘synthetic’ CBDC in the form of stablecoins. More generally, the discussions around the introduction of CBDCs should always include an evaluation of the possibility of considering well-regulated stablecoins as a viable (and possibly preferable) alternative.”

In addition, the aforementioned CSIS brief authored by CIA veteran DiPippo mentions multiple architectures the US government could adopt for their digital dollar, while realizing the advantages of a bank-issued deposit token. “A synthetic CBDC, is not really a CBDC at all, because the central bank would not be issuing the digital currency. A synthetic CBDC is a stablecoin with a twist: the issuing financial institution would back its stablecoin with reserves at the Fed.” He then noted that “A synthetic CBDC, or a system permitting the issuance of multiple fully backed dollar stablecoins, would be as safe as a CBDC while offering more private-sector competition and innovation.” In November 2021, the President’s Working Group on Financial Markets (PWG), the Federal Deposit Insurance Corp. (FDIC) and the Office of the Comptroller of the Currency (OCC) released a joint report on stablecoins, which highlighted that stablecoins could improve the US payment system but could also create financial risks if left unregulated. In general, realizing any benefits from stablecoins would require government regulation.

In prepared remarks this October, Barr stated “research is currently focused on end-to-end system architecture, such as how ledgers that record ownership of and transactions in digital assets are maintained, secured, and verified, as well as tokenization and custody models.” Barr also made the claim that any USD-denominated token “borrows the trust of the central bank,” and thus “the Federal Reserve has a strong interest in ensuring that any stablecoin offerings operate within an appropriate federal prudential oversight framework, so they do not threaten financial stability or payments system integrity.” Due to the popularity of and volume present in both the Treasury and stablecoins markets, there are currently many private banks attempting to digitize the securities market by creating a synthetic deposit token that acts like Treasuries.

In addition, the recent push in the US toward regulated stablecoins/deposit tokens and away from a direct-issued CBDC has other motives. While this push is at least partially motivated by the “bad reputation” that the term stablecoin has developed in the aftermath of the TerraLuna fraud in early 2022 and subsequent scandals in the crypto industry, commercial banks – including those that back Fluent Finance, R3 and their equivalents – want to issue the stablecoins/deposit tokens themselves in order to continue fractional reserve banking.

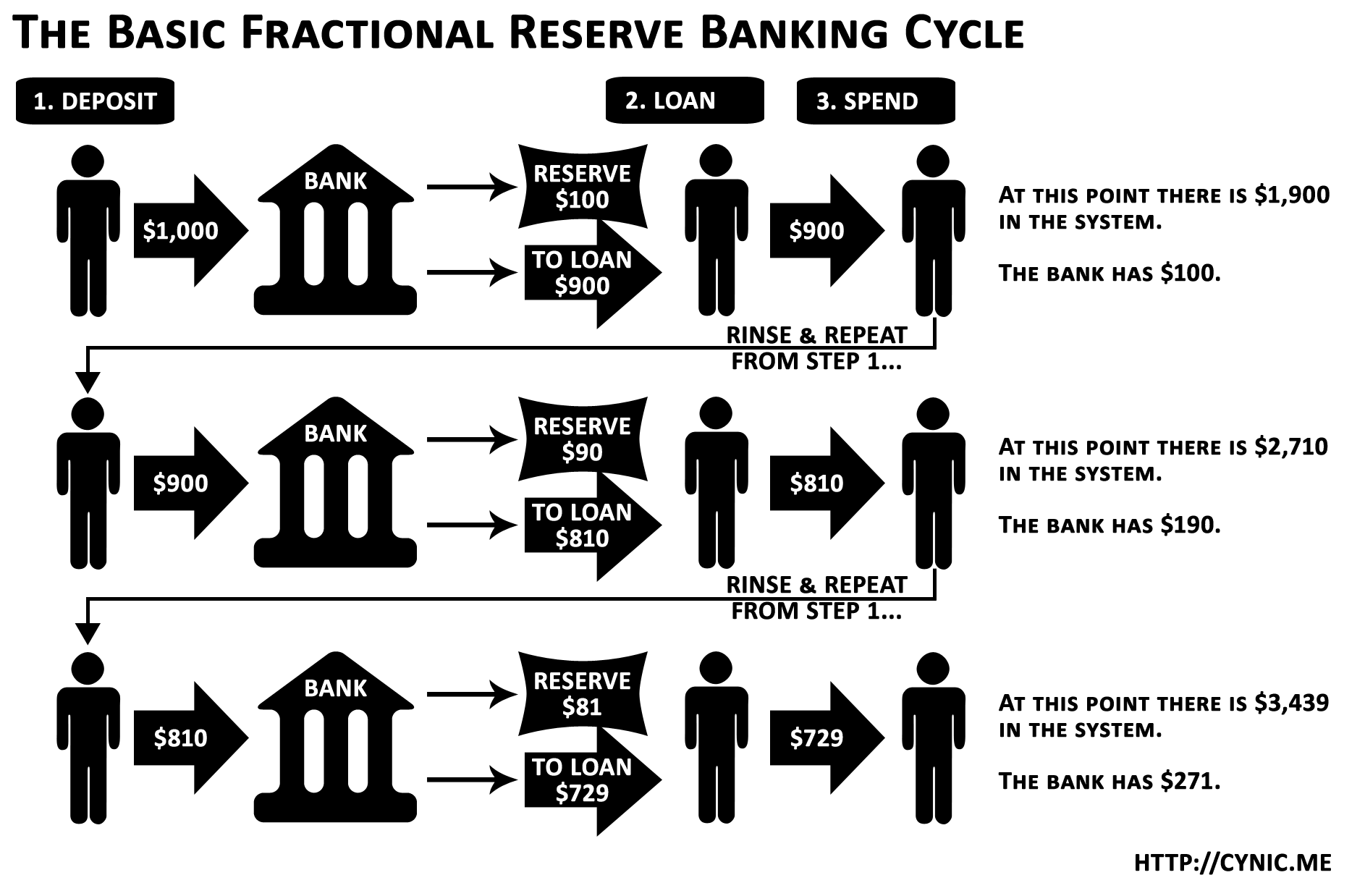

Fractional reserve banking, long controversial due to its role in facilitating bank runs and bank insolvency and characterized as some as little more than embezzlement, has long been a cornerstone of the US banking system. However, the current stablecoin paradigm, including that formerly embraced by Fluent Finance, have fallen out of favor with commercial banks as the 1:1 peg means that banks would have to hold onto equivalent reserves for every coin/token issued. In fractional reserve banking, banks engage in “credit creation” by loaning out the bulk of the money deposited by its customers and are unable to immediately (or even quickly) redeem customers’ money upon request – the entire purpose of the 1:1 ratio that characterizes most of today’s stablecoins. For banks to continue “business as usual”, the issuance of stablecoins and deposit tokens must come under their purview, as opposed to existing stablecoin issuers or even the Fed. Fluent Finance, as a company heavily influenced and guided by powerful commercial banks, is clearly positioning itself to be a key part of this bank-led digital dollar system.

In January 2023, Fluent’s Bradley Allgood told CoinDesk how the United States has been establishing its preference for a private-public model. He specifically pointed to the Federal Reserve Bank of New York and highlighted its initiatives in testing deposit tokens backing digital dollars for wholesale transactions in collaboration with major banks:

“When you look at the Fed of New York and what they have been doing in their innovation offices, this has been setting the standard, with all of it leaning towards wholesale, tokenized deposits or tokenized liability network settlement between bank to bank.”

During much of 2022, and particularly the timeframe in which Fluent Finance was forging its early partnerships including with Farmington/Moonstone, the behind-the-scenes push to create a synthetic CBDC for the US dollar in the form of regulated dollar-pegged stablecoins and/or deposit tokens was well underway. Fluent, from its earliest days, has sought to develop this synthetic CBDC and make it interoperable with any future direct-issued CBDC from the Federal Reserve while also exporting this synthetic dollar CBDC to the Global South. In light of the company’s (and US+’s) trajectory, it now makes sense to revisit the most likely motivation behind Moonstone’s partnership with Fluent prior to FTX’s collapse as well as the likely real goal behind Farmington’s transition into Moonstone.

The Bankman-Fried Stablecoin That Almost Was

Prior to the collapse of the Sam Bankman-Fried-led exchange FTX, there was already considerable speculation about the unusual relationship between FTX and its subsidiaries, Deltec and the dollar-pegged stablecoin Tether (USDT). For instance, nearly a year before FTX went under, Protos reported that “over two-thirds of all Tether minted across multiple years went to just two crypto companies”, one of which was the FTX-linked Alameda Research, the same Alameda Research that would later pour millions into Farmington State Bank during its suspect transition into Moonstone. Earlier that year, Alameda executive Sam Trabucco essentially admitted on Twitter that Alameda would use its massive holdings of USDT to maintain USDT’s peg to the US dollar (something also admitted by former FTX executive Ryan Salame). By October of 2021, Alameda had been issued almost $37 billion worth of USDT and had immediately forwarded $30 billion of that to FTX. Around that same time, FTX issued a $50 million loan to Deltec, which was a key bank for FTX and still is for Tether and whose chairman, Jean Chalopin, had recently acquired Farmington State Bank.

Over the next several months, Alameda Research and Sam Bankman-Fried himself would pour many millions into the Chalopin-controlled entity, making Farmington/Moonstone the newest entity of the Deltec-FTX-Tether nexus. This brings us to the big question: If Deltec and FTX were so close to Tether, why was the bank they controlled – Farmington/Moonstone – seeking to partner so intimately with another US dollar-pegged stablecoin – Fluent Finance’s US+?

For several years, and now more than ever, Tether has been under heavy scrutiny from US authorities, particularly the DOJ, and – given the US government’s push for regulated stablecoins/deposit tokens in lieu of a direct issue CBDC – it’s possible that Tether may not make the cut once those regulations finally come into force (though Tether’s recent overtures to US authorities and Congress obviously seek to prevent that). Tether, along with Deltec and quite obviously FTX, have long been suspected of engaging (or in FTX’s case, proven to have engaged) in bank fraud and a series of illicit financial activities. It seems as though powerful forces deeply tied to Tether, namely Chalopin and Bankman-Fried, were seeking to use Moonstone and its partnership with Fluent’s US+ the way the FTX web of companies/banks had used Tether. This would have presumably allowed them to continue their same shady financial machinations under the coming regulatory paradigm.

Notably, in late October 2022, three days after the Chalopin/Bankman-Fried-affiliated Moonstone partnered with Fluent Finance, Sam Bankman-Fried stated that FTX was due to announce the now bankrupt exchange’s collaboration with an unspecified stablecoin “in the not-too-distant future.” One wonders if the millions in political donations made by Bankman-Fried (and potentially those made by FTX executive Ryan Salame) in 2022 were aimed at wooing politicians to favor the planned FTX-affiliated stablecoin as a frontrunner for the coming “digital dollar” paradigm.

In other words, the goal was apparently to have the same group of actors transition from the “untrusted” Tether stablecoin to the “trusted” US+ stablecoin. The fact that Fluent Finance, whose co-founders include the alleged inventor of CBDCs and which was heavily influenced from the start by powerful commercial banks, claims to be a “trustworthy” alternative to Tether is deeply undermined and frankly unbelievable given that they would agree to allow the same untrustworthy actors deeply involved in Tether’s questionable minting activities (and FTX’s brazen fraud) to mint their “regulatory compliant” and “trusted” US+ stablecoin.

The Public-Private Digital Dollar

Following the collapse of FTX, and later Moonstone, Fluent Finance has continued in pursuit of its ultimate goal – to create a “trusted” stablecoin and stablecoin protocol on behalf of the commercial banking giants it was always intended to serve. In a September 2023 op-ed for Cointelegraph tellingly entitled “CBDCs could support a more stable economy – if banks run the show,” Allgood made his allegiances clear. In that article, Allgood writes that “employing CBDCs in an attempt to undercut, circumvent or cannibalize the entire commercial banking sector is as much a pipe dream for efficiency maximalists as it is a recipe for failure.” “Commercial banking will not be left in the dark ages,” he also claims.

In his defense of the commercial bank status quo, Allgood came out against the existing stablecoin paradigm in a recent interview with the IB Times, speaking in favor of bank-issued and regulated stablecoins backed by deposit tokens. “Stablecoins have not panned out the way most expected three years ago.” According to Allgood, deposit token models are now “emerging from the pack” of existing stablecoin issuance as the “most promising stable-valued digital assets.” He goes on to politically clarify that “stablecoins are not the bad guys…just the best effort from a previous era.” In this interview and also the Cointelegraph article, Allgood makes it clear that Fluent Finance not only possesses the necessary digital infrastructure, but also the institutional connections to keep private capital creation in the hands of commercial banks via deposit token architecture.

Allgood also told the IB Times that “the sticking point with stablecoins is that their issuers are essentially lean startups…When you consider the inherent security risks, frequent depeggings and compliance issues, it’s not difficult to understand why stablecoins have had no success whatsoever picking up traction in traditional use case scenarios.” The argument for moving the reserves of stablecoins back into the hands of the US banking system under the guise of further stability seems logical only until one remembers that Allgood’s favored custodians are the fractional reserve banking industry –– who would be able to engage in this controversial practice at a much larger scale under this new paradigm. Banking the unbanked –– a common trope from the stablecoin industry –– also sounds good in theory, as long as you ignore who gets to actually do the banking.

“If all goes well,” claims Allgood, “the global adoption of CBDCs will marshal a new financial paradigm where central banks implement superior monetary policy at the wholesale level while allowing commercial banks to do what they do best at the retail level with stablecoins and deposit tokens.”

While many rightly fear the danger to individual freedoms presented by government-issued CBDCs, this is not the paradigm being brought into focus by former Moonstone partner Fluent Finance or other key actors in building out the future of government-approved digital currencies. Instead of giving central bankers complete control over your finances in terms of surveillance and programmability, it will be the big Wall Street banks –– who in the US, own the Fed anyway – that will do the programming and surveilling. The further blurring of the public and private banking sector remains a powerful tool of obfuscation for the digital dollar system to skirt constitutional violations of customer rights in the form of warrantless asset seizure and data harvesting by a private sector that fully collaborates with the public sector. The digitization of the dollar, and the Treasuries that back them, leverage the databases of blockchains to not only demonstrate reserves of deposits, but also to track the users of the system. “The FX settlement process needs increased transparency and traceability”, R3 CEO David Rutter once explained. Rutter then boasted that his company “is fit to deliver on both counts.”

The simulated fear of governments and central banks programming your currency to expire will be conveniently eased by a public rejection of a directly-issued CBDC in the US by the Fed. The upholders of the status quo hope that the realities of this false victory, and the stablecoin/deposit token system to be implemented in lieu of a direct-issue digital dollar, will go unnoticed by the American public, particularly those segments of the population already wary of CBDCs. Whatever excuse or justification is given to move the US – and much of the world – into this new financial paradigm, rest assured that the same old bankers and companies – including those who came under scrutiny as part of the FTX scandal – will not only maintain, but gain, unprecedented control over the financial activity and behavior of every American and whoever else they decide to dollarize.

Ha, ha! Meet the new dollar, same as the old dollar! Same thievery and usury with a bit more twist to the currency wizard. When we the people choose to undo all this by dealing directly with one another, we will see that a profound new understanding and consciousness has been realized. Until then, let the pennies roll where they may.

on every “dollar”….”IN GOD WE TRUST”! No surer sign the devil is coming to collect on all the sins made in God’s name!

Thank you this, I learned a lot. It was very informative and terrifying

We live south of Spokane, WA. Not too far from Farmington. I cannot recall any local news coverage regarding this topic.

This is an astonishingly well researched piece and outstandingly good at explaining the role of so-called stablecoins in terms of maintaining dollar hegemony – and US government policy enforcement. The extent of R3’s relationship with Fluent is revelatory (and, consequently, with FTX’s stablecoin ambitions). But it does show the murky world that CBDCs are creating. The only comforting thing is that a dollar-denominated stablecoin/CBDC world is just one of several plays at work. It’s far from a slam-dunk as yet.

Wow, such a long read, but worth every time spent.

Thanks for this detailed and enlightening writeup

Whitney is probably a bit naïve about bitcoin, government’s view currency as the Devine right of kings and government and could just ban bitcoin in the future as economist Martin Armstrong thinks. If the US government voted next year to ban bitcoin and force conversion to US dollars they could just send the FBI out to seize all the servers and put pressure on other countries to also ban it. China already did ban crypto currencies.

Excellent!