Following the passage of legislation last year, the U.S. Department of Justice (DOJ) had to reluctantly publish a considerable amount of its Jeffrey Epstein-related documents, colloquially known as the «Epstein Files.» These files, estimated by some to represent as little as 2% of the Department’s Epstein-related documentation, do not offer a complete picture of Epstein’s activities as they are largely centered on emails from a single Gmail account used by Epstein: jeevacation@gmail.com. The email address appears to be primarily associated with Epstein’s activities while he was staying at his private island, Little Saint James, located in the U.S. Virgin Islands (USVI). However, the released emails contain many interesting revelations about key aspects of Epstein’s activities as well as his connections to prominent people who were intimately involved in his USVI operations.

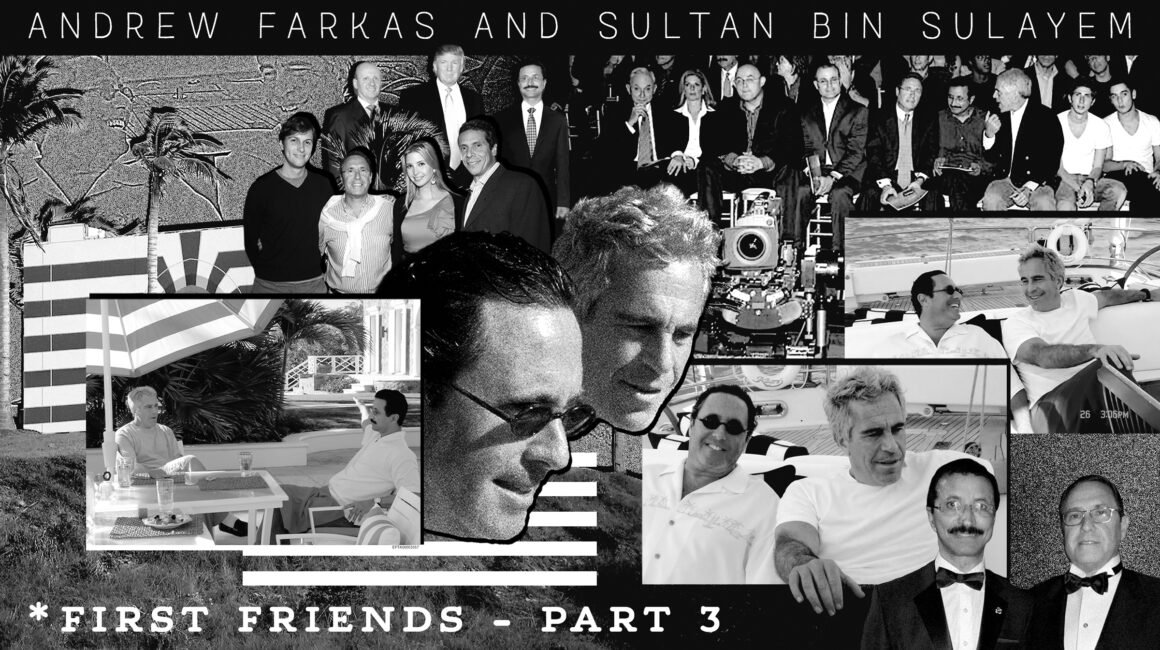

In this final installment of First Friends, a series that has examined figures with considerable overlaps between Jeffrey Epstein and the Trump family, a key nexus of Epstein’s activities, specifically in the USVI, has been illuminated by the recent document releases. It comprises Epstein, the Emirati elite Sultan Ahmed bin Sulayem (Sultan bin Sulayem or bin Sulayem in the remainder of this article), and New York businessman Andrew Farkas. Sultan bin Sulayem is best known for controlling a significant portfolio of Emirati government-owned assets, particularly in freight and the maritime industry, with important holdings in logistics globally as well as major real estate holdings in the United States and beyond. He recently became the subject of national media scrutiny when his name was redacted by the DOJ in an exchange with Epstein, whereby Epstein told him he «loved the torture video» that Sultan bin Sulayem had sent him. The DOJ has provided no further information about the «torture video.»

Sultan bin Sulayem is the long-time and close business associate of Andrew Farkas, a New York businessman whose family’s ties to Epstein date back to the 1980s. Farkas has extensive ties to fraud that was, and likely still is, rampant in the Department of Housing and Urban Development (HUD) during the 1990s. He later cultivated strong ties with the former HUD Secretary who once pursued him, former New York Governor Andrew Cuomo. After Cuomo left HUD, Farkas arguably became his most important source of campaign financing while also employing Cuomo in the private sector in between his stints in New York state and local government. As will be explored in this article, Farkas introduced his friend Sultan bin Sulayem to prominent figures in New York real estate, such as Donald Trump, and boasts extremely close business ties to Trump’s son-in-law, Jared Kushner, and to the Kushner family’s business interests. Importantly, Farkas and bin Sulayem seem to have played a key role in forging the Trump family’s initial ties to the UAE, whose government has come under scrutiny for its questionable investments in Trump-linked companies in recent years.

How Epstein first encountered Andrew Farkas and Sultan bin Sulayem is unclear, but they were first photographed together in 2005, earlier than previously reported. This article will show that Epstein and his broader network, including offshore financial institutions tied to the Maxwell family, appear to have worked to enable UAE business interests to take over key aspects of American maritime infrastructure. This later resulted in a national security scandal that involved top officials in the George W. Bush administration. In the years after, Farkas helped Epstein develop key aspects of the infrastructure he used and abused in the USVI to facilitate his trafficking activities, with bin Sulayem also offering assistance to help Epstein cover his tracks in major USVI real estate purchases. The evidence contained in this article makes it clear that Farkas and bin Sulayem warrant further investigation regarding Epstein’s trafficking and other illegal activities. However, given the DOJ’s willingness to redact bin Sulayem’s identity on at least one disturbing email, and the close ties of Farkas to the Trump and Kushner families, who also have major Emirati business interests, it seems clear that a federal investigation of these two figures and their ties to Epstein is unlikely.

A Farkas Family Affair

Andrew Farkas was born into a wealthy New York family, with his grandfather having founded Alexander’s department store, and he attended the elite Trinity School. There, according to the New York Times, he formed “a close circle of friends – many of them scions of other New York business families.” With classmates from Trinity, he founded his first company, which focused on database management, at age 16. He later attended Harvard University, where he spent his summers working for the London Metals Exchange as well as Salomon Brothers, which he joined full-time shortly after graduating. He left relatively soon after to begin building his real estate empire, which started with his founding of Metropolitan Asset Group in 1984 after he secured a $60,000 loan with his family’s help. Farkas had pitched his vision for Metropolitan to his family, describing that the idea “was to put the family’s resources into securitized real estate transactions and then draw in other people the family knew who already were investing in real estate but were having to pay high fees.” Farkas later described Metropolitan as “a real estate investment banking firm that specializes in working with distressed limited partnerships.” By 1987, Metropolitan claimed to manage over $250 million (over $715 million today) “on behalf of itself and its affiliates.” By 1989, the company had completed nearly $750 million of asset restructuring.

Over the next few years, Farkas set his sights on U.S. Shelter, a major apartment management company and player in a variety of real estate markets. Farkas’ interest was publicly reported in 1990 alongside reporting detailing U.S. Shelter’s significant financial troubles, as it was estimated to have hemorrhaged $52 million over the previous four years. This was largely due to the 1987 downturn, which pummeled real estate markets. Even Farkas’ firm Metropolitan fell into financial trouble, but Farkas later claimed to have “stuck it out” to become a “white knight” in the 1990s. In reality, Farkas’ “sticking it out” was only possible thanks to the $5 million he received from his wealthy family, which he used to create the Metropolitan-associated Insignia Financial Group in 1990. True to his initial vision for Metropolitan, Farkas’ family not only backed his firm but also brought 65 to 70 other families with them. Farkas would use this network of his family and their friends to gain “access to the highest echelons of management at virtually every financial institution and expertise in securitized real estate.”

Flush with cash from his family and their friends, Farkas created Insignia Financial Group, with the apparent intention of acquiring U.S. Shelter. As will be discussed in greater detail in the next section, Farkas’ recapitalization efforts on behalf of U.S. Shelter were designed to set the stage for his takeover of the company not long after. The merger between Insignia and U.S. Shelter was sealed in 1991, a year after Insignia was created. By 1992, the resulting company had become “the second largest property management company” in the country. A year later, in 1993, they went public with the help of a Lehman Brothers banker named Robert Lieber. Lieber later went on to be New York’s deputy mayor for economic development before joining Farkas’ Island Capital years later.

As time went on, it became clear that Farkas’ real interest in acquiring U.S. Shelter via Insignia was to gain access to a lucrative, American taxpayer-subsidized money spigot: grants and subsidies for low-income housing issued by the U.S. Department of Housing and Urban Development (HUD).

Andrew Farkas already had some connection to HUD, since his uncle, Jonathan Farkas, had served as the government-sector representative to HUD’s manufactured home advisory council from 1987 through 1988, stepping down a year before the formation of Insignia. Such «revolving door» relations would soon become ubiquitous in the fraud-soaked world of HUD contracting, and Farkas, through his relationship with U.S. Shelter, became linked to a cabal of notorious HUD fraudsters.

Wading into a Cesspool

In its most egregious instances, HUD fraud relied on a dense web of home building companies, real estate investment trusts, and law firms. These entities frequently overlapped with the looting of America’s savings and loans industry and the questionable financial practices associated with Drexel Burnham Lambert’s junk bonds. A veritable leviathan, the reach of this fraud machine extended to the families of powerful American politicians and the intelligence community.

One starting point for tracing this maze is the first company Farkas’ Insignia acquired, U.S. Shelter. U.S. Shelter was founded in 1972 by N. Barton Tuck, Jr., who also acted as the company’s longtime president. $10,000 in seed funding had come from Buck Mickel, the head of a major South Carolina-based construction corporation called Daniel International. This financial relationship cemented a deep interrelationship between U.S. Shelter and Daniel International, as summarized in a 1987 lawsuit against U.S. Shelter:

[Buck] Mickel was chairman of Old Shelter’s Board of Directors at the time of the reorganization and became Chairman of New Shelter’s Board of Directors when the reorganization was consummated. Mickel was vice chairman of the Board and member of the Office of the Chief Executive of Fluor Corporation. He previously served as president and vice chairman of the Fluor Corporation, a Fortune 500 Company. He is also a director and former chairman of Daniel International Corporation which was acquired by Fluor Corporation in 1977. Mickel has served on the boards of numerous corporations and universities. He is active in various community activities in Greenville.

In 1977, the same year that Fluor absorbed Daniel International, U.S. Shelter crossed paths with a bank that would later re-emerge during the BCCI affair. In April of that year, U.S. Shelter acquired H.G. Smithy, a large Washington, D.C.-based real estate management company, from Financial General Bankshares (FGB). Within months, FGB became the subject of a covert takeover by the Bank of Credit and Commerce International (BCCI), the sprawling, shadowy banking institution that had been established with the aid of the CIA and which moved money for a seemingly infinite parade of intelligence agencies, terrorists, financial criminals, and drug traffickers.

Daniel International’s real estate subsidiary was Daniel Realty Corporation, which separated from Fluor in the 1980s and became an independent company. Charles Tickle served as an executive for Daniel Realty, both during and after Fluor’s control of the company. He, too, boasts a series of intriguing ties. For instance, during the 1980s, Tickle joined the board of an important company, SICO-Curaçao. This was an offshore corporate vehicle and “player in real estate worldwide” that was, in fact, just one node in a web of subsidiaries, holding companies, and joint ventures cloaked in a pantheon of shell companies. This network of entities was overseen by its parent entity, SICO, the Saudi Investment Corporation.

Established in 1980, SICO was controlled by Yeslam Bin Laden (the half-brother of Osama Bin Laden) and other members of the Bin Laden family. Tickle ended up associating with Yeslam due to the fact that Daniel and SICO had been working together on a number of real estate development projects across the United States. Steve Colls recounts in his book The Bin Ladens: An Arabian Family in the American Century that:

They formed offshore corporations to serve as financing vehicles, with Tickle and Yeslam sometimes named as directors. The only real mystery, Tickle recalled, was whose money Yeslam was actually investing—his, or that of other members of the Bin Laden family, or that of other Saudi investors, or money from some other source. “That was always such a secretive thing,” Tickle said. At the time, as a business issue, “We could have cared less.” For Daniel Corporation’s purposes, all investment funds were the same; Yeslam had access to quite a lot of cash, and there was no reason for Tickle to believe that it was coming from improper sources.

Despite Tickle’s supposed lack of interest in the source of funds for their real estate ventures, there are reasons to raise questions about the money that SICO and Daniel were pouring into the United States. SICO’s expansive and convoluted network of companies intertwined with those of BCCI in numerous ways (making the cross-over between U.S. Shelter, closely tied to Daniel and Fluor, and banks targeted by BCCI in 1977 all the more intriguing). Other links existed between SICO and the financial networks used by the CIA for its covert funding of the Mujahideen in Afghanistan, and to drug traffickers and money launderers operating in the Afghanistan-Pakistan region.

The CIA connection is particularly interesting, as it quickly becomes apparent that the funding of the Mujahideen was not the only covert operation that SICO had brushed up against. The corporate structure of SICO was set up by the Swiss attorney Baudoin Dunand, who later served on SICO’s advisory board. Researcher Kevin Coogan found that Dunand was involved in another entity, Tyndall Trust, which former American tax attorney Willard Zucker managed. Zucker, in turn, was the man tapped to serve as the financial manager for “The Enterprise,” the private intelligence network tied to the CIA and Israeli intelligence that was established to manage the complicated plots and machinations at the heart of the Iran-Contra affair.

Fluor, the construction giant that had acquired Daniel International — and which interlocked with U.S. Shelter via Buck Mickel — also appears to have been involved in Iran-Contra activities in some capacity. This revelation came from journalist Gary Webb’s reporting on how the CIA-backed Contras were involved in the cocaine trade and had helped fuel the explosion of crack in urban Los Angeles in the 1980s. Of particular interest to Webb was Ronald Lister, a former police officer turned “cocaine hauler and money launderer” for Jose Blandon, one of the right-hand men for Panamanian strongman (and CIA asset) Manuel Noriega between 1980 and 1981.

Around the time he started working with Blandon, Lister formed a company called Pyramid International Security Consultants in California, whose purpose was to “sell weapons abroad” — particularly to the Contras through El Salvador. Webb learned that Lister himself had a CIA contact, Bill Nelson, who had previously served as the CIA’s deputy director of operations. However, at the time that Nelson was operating under a business cover for the CIA, he had been vice president of security and administration at Fluor.

Lister’s contact with Nelson reportedly took place while Nelson was working for Fluor, and the arms trafficker reportedly made frequent visits to the company between 1982 and 1983. Nelson, interestingly enough, had joined up with Fluor in 1977, the same year that Fluor had purchased Daniel International.

U.S. Shelter, meanwhile, embarked on an incredible expansion — and the development of an increasingly complicated corporate organization — in the years after 1977. A string of acquisitions saw the company gobble up smaller property management companies across the United States (such as Gold Crown Properties in Kansas City) and dip into banking by buying Malibu Savings & Loans in California. Subsidiaries were established, including U.S. Shelter Trust of Massachusetts, U.S. Shelter Corporation of South Carolina, U.S. Shelter Corporation of Delaware, etc. These were shuffled around and later merged in various combinations.

As previously mentioned, however, U.S. Shelter was flailing by the late 1980s. Suffering under the burden of “bad real estate investments and failure to meet new capital requirements for a savings and loan institution it owns,” the company embarked on a recapitalization plan. Key to this recapitalization was Andrew Farkas and his Metropolitan Asset Group. The plan ensured that Metropolitan would end up with a significant chunk of U.S. Shelter stock alongside Lambert Brussels Real Estate Corp., an American real estate arm of the Belgium-based Groupe Bruxelles Lambert.

Lambert Brussels Real Estate’s chief, Joseph Murphy, was also a member of the executive committee of Drexel Burnham Lambert, the major investment bank most infamous for being the seedbed for Michael Milken’s junk bond operations. Here, too, one finds the fingerprints of clandestine activities and covert operations. According to Ari Ben-Menashe, Drexel was one of the laundering mechanisms for the funds generated by the American and Israeli arms sales to Iran that were central to the Iran-Contra affair. This arms money, states Ben-Menashe, “added to Drexel’s stature, and Drexel’s share of the profits from deposits helped it underwrite huge quantities of junk bonds.” Some close Epstein associates, such as Leon Black, had been top executives at Drexel prior to its 1990 bankruptcy.

The recapitalization plan didn’t seem to function well enough for U.S. Shelter to recover, so a new scheme was put in place. U.S. Shelter would simply cease to exist, and its assets (minus its beleaguered California savings and loan institution) would be transferred to his new company, Insignia Financial Group.

When Farkas and Insignia finally acquired U.S. Shelter in early 1991, the primary goal was to take control of properties that had been owned and managed by A. Bruce Rozet. Once described as “one of the nation’s largest owners of subsidized housing,” Rozet had been the owner of the Associated Financial Corporation of Los Angeles, California. He was also a crook of the highest order: in February 1990, HUD suspended him from obtaining lucrative contracts due to his involvement in extensive fraud.

Rozet had been diverting HUD funds intended for maintenance and the upkeep of HUD-subsidized properties for personal use. In other instances, he tapped HUD funding for empty homes, all the while fudging paperwork to make them appear occupied. A blitzkrieg of lawsuits soon followed in Rozet’s wake, adding misdeed upon misdeed — insurance fraud, kickback schemes, and the like. In April of 2001, Rozet admitted guilt to a number of fraudulent activities and was fined $10.2 million.

Andrew Cuomo, who served as assistant secretary of HUD from 1993 through 1997 and as secretary from 1997 to 2001, described Rozet as “one of those ‘bad landlords who used HUD programs like personal ATM machines to enrich themselves and rip off the American taxpayer.’” Yet, Cuomo would soon work closely with Andrew Farkas, the man who ended up with Rozet’s properties through U.S. Shelter.

The HUD Fraud Octopus

When HUD began to unravel Rozet’s machinations, it demanded that the Associated Financial Corporation (AFC) “turn over the management of 79 properties to an independent firm, initially U.S. Shelter.” This was two months prior to Insignia’s formal acquisition of U.S. Shelter. However, as noted above, Farkas was already in the loop. He “consulted” with U.S. Shelter on their impending acquisition of the Rozet property portfolio and became privy to certain arrangements of a dubious legal nature that Rozet had engaged in. These involved a “payback” scheme, initially set up by AFC and later continued by Farkas, in which a portion of HUD-subsidized management fees would flow back to the property owners.

The AFC – U.S. Shelter – Insignia payback arrangement was discovered by HUD inspectors in 1995, leading to a joint HUD/Office of Housing/Department of Justice investigation into the companies, their financial arrangements, and properties under management. What they discovered was that HUD funds had not been used to maintain the properties, which had fallen into an extreme state of disrepair. Cuomo would later tell the Village Voice that the properties’ conditions were «despicable.» The Voice also reported that, when Cuomo visited one of these properties, he “’saw a broken pipe literally spewing human waste on the children’s playground.’ He said he saw children playing in it.”

In 1997, a lawsuit was filed against Insignia for “paying $7.6 million in kickbacks to the owners of 17 federally subsidized projects that Insignia managed.” Farkas paid an initial $5 million to HUD for diverted management fees, and in March 1998, Insignia paid another $2.4 million but declined to admit guilt. It then sold its residential units for a whopping $910 million. Not long after, in August of 2001, Insignia began making significant contributions to Andrew Cuomo, who had left HUD and was now running for governor of New York.

Cuomo lost the race. He first worked for the law firm of Fried Frank before taking a position at Andrew Farkas’ post-Insignia company, Island Capital, in 2003. There, he was paid an annual salary of $1.2 million.

This was not the first time a Cuomo had intersected with a Farkas. As the Village Voice recounts:

They [the 2001 contributions] were hardly the first Farkas contributions to a Cuomo; other members of the Farkas family, which used to own the Alexander’s department store chain, had contributed to the campaigns of Cuomo’s father, Mario, when he was governor. Mario Cuomo actually appointed Farkas’s father to the board of the state’s powerful Dormitory Authority in his final year in office in 1994, and Robin Farkas [Andrew Farkas’ father] became its chairman in 1995.

Farkas had other political ties beyond the Cuomo family. Through Insignia, his ties extended to the powerful real estate management companies and investment trusts that also drew on the HUD money spigot, and which had connections to that infamous American political dynasty, the Bush family.

In March 1998, right as Insignia was forking over millions in connection with Cuomo’s HUD lawsuit, Farkas was making major business moves. With the multimillion-dollar worth of fines on the horizon, Insignia unloaded its apartment portfolio to Apartment Investment & Management Company (AIMCO), a Denver-based real estate investment trust controlled by homebuilder and real estate manager Terry Considine. Around the same time that AIMCO was buying up Insignia’s portfolio, the company also found itself in hot water with HUD over its plans to repurpose HUD-subsidized properties to cater to higher-end clientele, thereby displacing lower-income renters.

Notably, Denver itself was a hotbed of HUD fraud. As investigator and journalist Rodney Stich recounted in his book Defrauding America:

A major segment of the HUD fraud was centered in the Denver area and committed by a group of closely related people and companies, who had close ties to the Reagan and Bush administrations. Numerous HUD officials left government to work for the Denver group that defrauded the American people of billions of dollars, much of which is hidden away in either offshore financial institutions or in secret locations throughout the United States. Philip Winn was one of the kingpins in the Denver group. He was a former HUD assistant secretary who joined the MDC group in Denver and became a key player in the HUD and savings and loan scandals.

A 1996 article by the Denver paper Westword confirms much of what Stich wrote, noting that former HUD assistant secretary Philip Winn “was part of what became known as the Winn Group, a collection of former agency officials turned developers who received more than $160 million in federal tax breaks and subsidies from HUD.” The article also notes that Winn was operating in the same business and social circles as the heads of MDC Holdings, owned by “mega-developer” Larry Mizel. MDC had been part of a complex “daisy chain” operation that involved Silverado Savings, Charles Keating’s Lincoln Savings, Drexel Burnham Lambert, and a number of other crooked financial institutions. The whole operation notably boasted exceedingly close ties to the Bush family, particularly to Silverado, where Neil Bush was a director.

To bring this full circle, Mizel hired Terry Considine — the owner of AIMCO, the company that purchased Insignia’s apartment portfolio — to run real investment trusts controlled by MDC.

There is also the case of NHP Inc., a Washington, D.C.-based apartment management and real estate company that, in the early 1990s, was one of the largest in the nation. The company had also built itself up through questionable activities involving HUD. Just a few short months before AIMCO purchased the Insignia apartment portfolio from Farkas, it purchased NHP, its real estate assets, and an associated company.

Shepherding the NHP sale to AIMCO was Michael Eisenson, the board member who represented the interests of NHP’s then-dominant shareholder: the Harvard Management Company, an investment company owned by Harvard University and the manager of the university’s endowment. Another curious place where Eisenson turned up as a board member — due to a large investment by Harvard Management — was Harken Energy. This obscure energy company counted George W. Bush as a major shareholder and board member. During the period when Bush was affiliated with the company, Harvard Management invested about $50 million in it.

Besides George W. Bush, Harken had significant ties to the intelligence community. Major shareholders in the company (predating Bush’s arrival) included an investor syndicate led by Alan Quasha, a New York attorney. Alan’s father, William Quasha, had been a licensed attorney in the Philippines, where he had close ties to figures involved in the infamous Nugan Hand Bank. Nugan Hand, run by several CIA and ex-military personnel, was deeply involved in the clandestine trade of arms and drugs.

While these elements might seem tangential to the world of HUD fraud that Farkas found himself entangled within, they may help explain a strange series of events in which Farkas made an appearance: the story of Catherine Austin Fitts and her company, Hamilton Securities. A veteran of Dillon Read & Co, Fitts had been recruited by HUD Secretary Jack Kemp in 1989 to serve as the Federal Housing Administrator. Her mandate was to reform “the scandal-ridden, fraud-plagued agency.”

After her stint at HUD, Fitts formed Hamilton Securities to clear out waste, redundancy, and economic abuse in the federal housing programs. Specifically, Hamilton was hired to help oversee HUD’s loan sales program, which was set up to shift delinquent mortgages from the government agency to private investors. What made Hamilton different is that, among other tools, the company implemented an online database and bidding software that helped establish an open market for the defaulted mortgages. By clearing these types of mortgages off their books, HUD would have been able to free up money that could then be used to lower the costs in other areas of its housing activities.

Such a scheme inevitably upset insiders who had been playing HUD for unsavory purposes for years. As Fitts would put it:

Hamilton’s efforts stood in the way of the «financial coup d’etat» – of engineering a mortgage bubble using federal mortgage fraud, of «disappearing» billions from federal accounts, and of a new wave of gentrification which would include the development of private prison companies financed with federal contracts.

Early opposition came from Michael Eisenson, the Harvard Management executive who sat on the Harken board (alongside George W. Bush) and was involved with HUD through NHP. He told Fitts that NHP disliked Hamilton because they “prefer[red] a bid process where we can win by ‘gaming it’ because we are ‘smarter.’”

Another opponent of Hamilton was Andrew Farkas. In addition to the loan sales program, Hamilton was brought in to consult with HUD on its “project-based subsidy” program — that is, subsidies for buildings that flow to the property owners and building managers. At the time, these subsidies were expiring, and HUD was deciding whether to renew the program or switch to a tenant-voucher approach, which issues vouchers to tenants to help them access low-cost housing and move without losing assistance.

In the midst of this debate, Farkas contacted Fitts at Hamilton and told her that “it was essential that all subsidies go to the owners of the properties in the form of ‘project-based’ assistance,” because tenants would use the voucher program to somehow “buy drugs.” The implications of Farkas’ statement are clear: his contact with Fitts would have coincided with the time when Insignia was embroiled in the payback scheme the company had willingly (and intentionally) inherited when it took over U.S. Shelter. Farkas simply did not want the HUD spigot to be turned off.

In October 1997, HUD fired Hamilton, sparking a protracted conflict that dragged Fitts and her company through the court system. Trumped-up charges and burying Hamilton in legal paperwork — a well-oiled and time-tested strategy — became the name of the game.

Is it a mere coincidence that within a year, both NHP and Farkas’ Insignia would be consumed by AIMCO in Denver, a company firmly entrenched in a complex network of HUD and savings and loan fraudsters connected to the highest levels of American political power? Whistle-blower Stewart Webb, an individual with significant knowledge of these white-collar criminal networks in Colorado, suggested that Fitts and Hamilton had been a “direct threat to the ‘Denver Boys’ — the Bush Crime Family’s money laundering operations based in Denver.” The HUD money spigot, according to Webb, was “a massive covert revenue stream for them.”

Who had been the person who fired Hamilton? The same man who had first investigated and then later went to work for Farkas: Andrew Cuomo. Yet, even before that, the first lawsuit had been filed by a company run by John Ervin, a former NHP employee.

Journalist Lucy Komisar has suggested that Farkas ultimately chose to back Cuomo so strongly because he benefited from Cuomo’s policies toward the end of his term as head of the Department of Housing and Urban Development under Clinton. She singled out Cuomo’s decision to fire Hamilton Securities Group, run by Catherine Austin Fitts, even though Hamilton had reduced fraud and helped create policies that had been applauded for benefiting homeowners and taxpayers. One of the biggest beneficiaries of Cuomo’s decision was Farkas’ Insignia. After firing Hamilton, Komisar notes, Cuomo’s HUD lost track of $17 billion, which was blamed on a company deeply tied to Clinton and then-Bush’s IRS Commissioner, Charles Rossotti. Subsequently, Rossotti was hired by the Bush family-connected Carlyle Group in 2002.

Farkas Goes to Dubai

Around the time Farkas began financing Andrew Cuomo, he also began forging ties overseas that would be critical not only to his career but to his future dealings and friendship with Jeffrey Epstein. In 2002, Farkas was introduced to Sultan Ahmed bin Sulayem, then head of the Dubai Port Authority (DPA). A few years later, in 2005, DPA merged with other Dubai-controlled logistics companies to form DP World, which bin Sulayem controlled and which later became Dubai World.

Farkas and bin Sulayem were first introduced by Sol and Howard «Butch» Kerzner, father and son hotel/casino magnates from South Africa. Mr. Farkas later told the Observer that “I was taken to Dubai by Butch [Kerzner] with a tremendous degree of frequency. Sultan and I became fast friends. We came to know each other very, very well.” A year after meeting bin Sulayem, Farkas sold Insignia and created Island Capital with the money from Insignia’s sale and other sources. He quickly began using his new company to develop marinas in Dubai “hand-in-hand with Mr. Sulayem,” per the Observer. Also in 2003, Farkas helped flood Dubai’s real estate market, in which Sulayem-controlled entities played an important role, with mortgage-backed securities (discussed in greater detail later in this article).

The Kerzner dynasty, responsible for introducing Farkas and bin Sulayem, was a controversial bunch. Sol Kerzner, once called “an unforgettable and important brick in the wall of [South African] apartheid,” had a long track record of accusations of bribery, financial crime, and using “apartheid to advance his business interests.” The Kerzners also owned Paradise Island, formerly a crown jewel of the mob and CIA-linked company Resorts International. They bought the island in 1994 from what remained of Resorts International after it was taken over by Merv Griffin, whose acquisition of the controversial company was fueled by the criminal bank Drexel Burnham Lambert and its junk bonds.

Kerzner also appears as “Sol Kersner” in Epstein’s “black book,” as does Gerard Inzerillo, who was COO of Kerzner’s Sun Resorts from 1991 to 1996 and president of the Kerzner Entertainment Group from 1991 to 2011. In the early 2000s, Inzerillo served as a founding advisory board member of the Clinton AIDS initiative, which Epstein helped launch, and was later put in charge of the Diriyah Gate Development Authority by Saudi Crown Prince Muhammad bin Salman (MbS), who was also known to have been very close to, and likely advised by, Epstein.

Sol Kerzner was also very close to New York real estate developer Donald Trump, now U.S. president. Kerzner once told the Forward that Trump “is a great friend” and “helped me at a time when South Africans were not well received.” Trump was fond of both Sol and his son, «Butch,» calling Butch a “great visionary” and “one of the few sons who was able to stand up in terms of talent to a great father.” Trump, as a major figure in the real estate scene, has long boasted close ties with Andrew Farkas, as he once did with Jeffrey Epstein, who was once commonly referred to in press reports as a New York-based «property developer.»

It seems that one of the main reasons Sultan bin Sulayem was interested in Farkas is that he could help connect Emirati interests to the elite New York circles that Farkas had long inhabited. According to Muneef Tarmoom, the former CEO of Istithmar — an investment firm owned by Dubai World — Farkas was “the connections man.” Tarmoom added that “He knew everyone in New York. Whatever introduction he did, he usually would get a cut on it.” After meeting bin Sulayem, Farkas would introduce him to Jeffrey Epstein. Epstein, bin Sulayem, and Farkas are all pictured alongside Leslie Wexner in the front row of the 2005 Victoria’s Secret annual televised fashion show, with Farkas and bin Sulayem clearly being Epstein’s VIP guests for the star-studded event. This was roughly three years after the first meeting between Farkas and bin Sulayem. It is also the earliest documentation of the relationship between the three men. For both bin Sulayem and Farkas, their relationships with Epstein would prove highly significant.

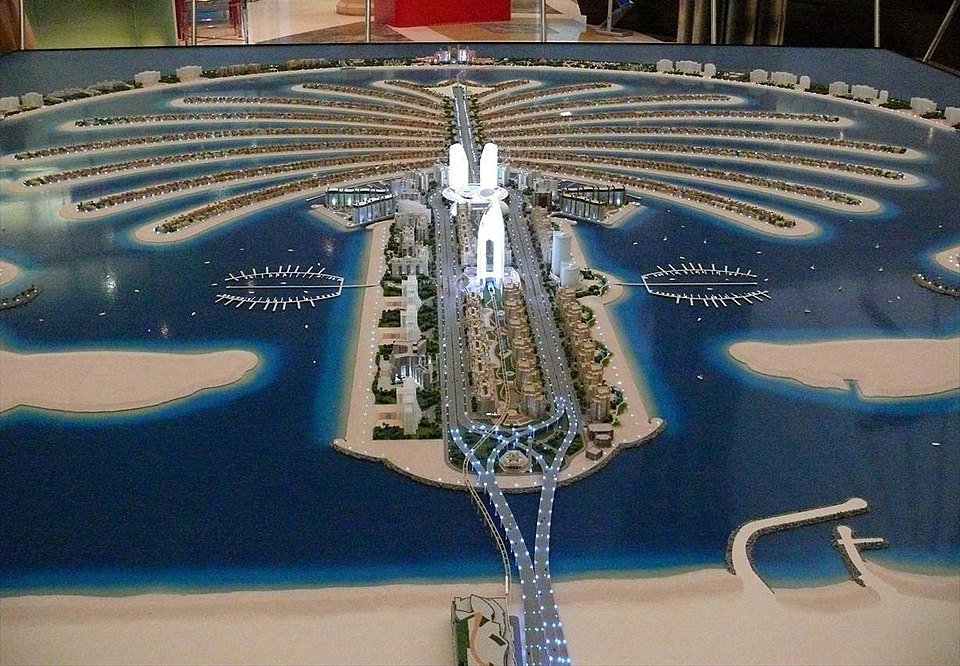

In addition to Epstein, Farkas also introduced bin Sulayem to Kerzner’s friend Donald Trump. Trump subsequently became involved in a joint venture with the Dubai World-owned real estate developer Nakheel on Dubai’s The Palm, the world’s largest man-made island, and later worked again with Nakheel to build the Trump International Hotel and Tower in Dubai. In the planning phase, Trump remarked on what would have been his family’s first venture in the Middle East and that the Nakheel development was the best real estate investment in the entire region, stating that “When I look at potential sites for real estate investment, I concentrate on ‘location, location, location’ – and this is the best location not only in Dubai but the whole of the Middle East.”

However, the Nakheel joint venture was rebranded as a Nakheel-owned project featuring only Trump family branding in July 2008, after Nakheel began reeling from issues related to the 2008 economic crisis (more on that soon, as Farkas seemingly played a role in Nakheel’s troubles). Oddly, in the midst of that crisis, Trump nevertheless hosted a large, celebrity-studded party at his Los Angeles estate, announcing the Nakheel-developed Trump Tower in Dubai in August 2008. The hotel and tower plans were also eventually canceled in 2011 due to Nakheel’s dire financial situation, though Nakheel promoted it up through 2013. However, plans to build it were relaunched just last year, this time with a Saudi-based real estate developer. Even though the initial ventures with Nakheel were delayed and later canceled due to the 2008 economic crisis, the Trumps appear to have maintained ties to Sultan bin Sulayem, who attended Trump’s inaugural ball in 2017 alongside Farkas. Sultan bin Sulayem’s son was also in attendance.

Farkas, the man who initially brought Trump’s business interests to the Gulf, perhaps deserves considerable credit for the close ties forged by members of Trump’s family to the UAE, which have proven very lucrative over the years, including during his second term. They have also featured prominently in allegations of pay-to-play and conflicts of interest during his presidencies.

One particular member of the Trump family who has clearly benefited is Trump’s son-in-law Jared Kushner. The Kushners, and Jared in particular, also notably boast long-standing ties to Farkas. For instance, Jared Kushner and Farkas were pictured together in 2011 at a “Masters of Real Estate” event, and in 2009 at the 80th anniversary party of the Montauk Yacht Club, which Farkas owns. In the 2009 picture, Jared, his wife Ivanka, and Farkas are pictured with Andrew Cuomo, whose gubernatorial campaign finances have long been closely connected to Farkas, as noted previously.

In subsequent years, the Kushner family would come to rely heavily on entities controlled by Farkas for important real estate deals. In a 2017 Bloomberg article titled “Kushners’ New York City Buildings Are Mostly Owned by Others,” it was noted that a key source of funding for the Kushner family’s real estate deals in New York was Farkas’ C-III Capital Partners. One example given was a 2015 deal for 16 apartment buildings, which was credited to the Kushners even though the majority of the funds for the buildings’ acquisition had come from C-III. Also in 2015, Farkas became an important investor in Cadre, a real estate start-up co-founded by Jared and his brother Josh. A few years later, in 2018, a Farkas-controlled firm again provided financial backing to the Kushners, this time for the $102 million purchase of two New Jersey apartment buildings. At that time, Jared Kushner was one of the key figures for UAE relations in the first Trump administration. As noted above, Farkas had attended the inaugural festivities for Trump a year earlier alongside his “frequent business partner” Sultan bin Sulayem and his son.

In 2023, Kushner became even more entangled with UAE business interests, particularly via his firm Affinity Partners, which raised more than $200 million from a UAE sovereign wealth fund. He and Steve Witkoff, whose family has its own dubious conflicts of interest with the UAE, have become the key point men for Middle Eastern affairs in the second Trump administration.

In addition to the Trumps and Jared Kushner, another Farkas-brokered connection for Dubai World was to the Drexel Burnham Lambert-linked corporate raider Carl Icahn. Icahn subsequently convinced Dubai World to invest billions in Time Warner during a failed takeover attempt. During this period, the Kerzners also partnered with Dubai World’s Istithmar to build an Atlantis resort on The Palm. Istithmar later helped lead the consortium that took Kerzner International private and ultimately ended up with 30% of the Kerzner family empire.

Preying on Ports

For DP World, and later its successor Dubai World, Farkas was much more than a “connections man.” He served as a major adviser and dealmaker for the conglomerate and also for other powerful figures in the UAE. He, along with Andrew Cuomo, whom he hired in 2003 to work at his firm Island Capital, advised developers in Dubai, including those tied directly to Dubai World, both in the UAE and abroad, with a particular focus on the USVI. The extent of Farkas’ ties to the USVI, as well as the extent of his direct ties with Epstein, is detailed in a later section of this article.

As previously noted, the year before Cuomo joined Island Capital, Farkas had been one of Cuomo’s top fundraisers for his unsuccessful gubernatorial bid in 2002, with Farkas subsequently playing the role of Cuomo’s top “money man.” Farkas’ involvement in Cuomo’s campaign financing would be a recurring theme throughout their long-lasting relationship.

During the Bush era, with Cuomo alongside him, Farkas also made significant property deals with Dubai World’s Istithmar, among others. For instance, Farkas partnered with Istithmar on several Manhattan real estate purchases as well as USVI marinas. Istithmar ultimately bought a 29% stake in Farka’s marina development and management company Island Global Yachting, which owns American Yacht Harbor –– the marina that Epstein would later co-own with Farkas.

Inconveniently for Farkas and his Emirati associate, Dubai World’s port-focused subsidiary, DP World, became the focus of a major national security controversy from 2005 to 2006. In 2005, DP World moved to acquire the British company, Peninsular and Oriental Steam Navigation Co. (P&O), which owned or leased terminals in many global ports, including six major U.S. ports: Baltimore, Houston, Miami, New Orleans, Newark, and Philadelphia. However, DP World’s attempts to acquire key U.S. infrastructure were even more extensive than these six ports, as they also sought to gain a foothold in the Port of Tampa, Florida, and key infrastructure near the Port of Charleston, South Carolina.

The P&O shares that facilitated DP World’s takeover attempt were systematically sold off during the 1990s and up until DP World’s successful acquisition in 2005. Many of these shares were incidentally sold off in connection with a money laundering scheme tied to Epstein-connected interests, particularly the family of Ghislaine Maxwell, Epstein’s long-time associate and accomplice. This P&O share sell-off is notably at the center of a recently filed lawsuit targeting HSBC, Barclays, and an «Epstein-linked Trust.»

The story of these P&O shares starts with a man named John Dick, who was linked by journalist Pete Brewton to the Denver-linked money laundering network discussed earlier in this article. In particular, Brewton linked Dick to the looting of the Denver-based Silverado Savings & Loan, where Neil Bush (brother to George H.W. Bush) served on the board and whose misappropriated funds were allegedly used to finance clandestine CIA activities. Brewton also connected Dick to other S&L frauds in Florida and Texas, particularly those involving the intelligence-linked Robert Corson, who also boasted close ties to George Bush Sr. When the money spirited out of these S&Ls was traced to the tax haven of Jersey, it was also revealed that Dick had been living in Jersey since at least the mid-to-late 1970s.

According to a copy of the complaint of the aforementioned lawsuit provided to Unlimited Hangout, one of the trusts set up for Dick’s children, but from which John Dick was explicitly excluded at his wife’s behest, included a major position in the company European Ferries. In 1995, one of the trustees — Barclaytrust, a Jersey-based trust division of Barclays — retired, transferring control to another Jersey company called La Hougue Boete. La Hougue was formed in 1984, and the company’s ultimate beneficial owner was none other than John Dick. This is despite the fact that he was meant to be entirely excluded from the trust’s management. Unfortunately for Dick’s children, La Hougue was a money laundering enterprise and, even though their father was at the helm, this company would soon strip their trust of its assets, including their major position in European ferries.

When European Ferries was acquired by and then merged with P&O, a deal finalized in 1987, the stock in European Ferries in the Dick children’s trust became P&O stock. According to a source with direct knowledge of the legal case in question, the John Dick-controlled La Hougue used a Jersey-based shell company called Cannon Nominees to progressively sell off this P&O stock, with none of the proceeds from those sales flowing back to the trusts in question. This sell-off created the opening that DP World later exploited to take control of P&O.

While the lawsuit brought by one of Dick’s children focuses on La Hougue’s activities related to P&O stock, La Hougue and its shell company Cannon Nominees were intimately connected to the finances of the Maxwell family, specifically Kevin and Ian Maxwell. La Hougue facilitated several murky transactions on behalf of the Maxwells, many of which involved shares in Kevin Maxwell’s company Telemonde. UK press articles have noted that after the death of his father, Robert Maxwell — a brazen financial criminal and spy — Kevin sought to become his «father reincorporated» and continued aspects of his espionage-tinged activities. During the period when Kevin and Ian were tied to La Hougue, Kevin served as director of 81 companies, only 32 of which survived, while Ian — in 2001 — was the director of 31 companies, four of which faced insolvency.

A key figure in the Maxwell family’s activities regarding La Hougue was George Devlin, a British lawyer and private investigator whose legal clients included the organized crime figures, the Kray twins, and Lord Lucan. Lucan was a member of the notorious Clermont Club, a gambling enterprise with close associations to Robert Maxwell, British intelligence, and organized crime. Lucan infamously disappeared in the mid-1970s after coming under suspicion for the murder of his children’s nanny and the attempted murder of his wife. Devlin created the UK property company Chelsfield alongside his close friend, Elliot Bernerd, which engaged in joint ventures with P&O. Perhaps more interesting is that Kevin Maxwell served as a front for Elliot Bernerd in at least one deal, revealing the interconnectedness of this particular group.

Notably, the Epstein-focused investigation of U.S. Congressman Ron Wyden (D-OR) has also led to scrutiny of La Hougue, as it is one of the institutions (#20) on the list of individuals, entities, and banks that are the focus of Wyden’s bill, the Produce Epstein’s Treasury Records Act.

The key takeaway from this legal case, as it relates to this article, is that a Maxwell/Epstein-linked money laundering enterprise directly facilitated the sell-off of P&O stock that enabled DP World’s takeover of P&O. This is particularly relevant given that, as will be discussed shortly, Epstein was first photographed in November 2005 with DP World’s then-chair bin Sulayem while its acquisition of P&O was still being finalized.

Although the involvement of La Hougue in the DP World takeover of P&O was not known at the time, the acquisition led to a major public outcry. These concerns were centered around the UAE’s ties to 9/11 money flows and the turning over of the ownership of the United States’ most important ports to a foreign country at a time when the War on Terror, and its propaganda machine, was still on full tilt.

The initial outcry soon became frenzied when it was revealed that the Bush administration had approved the deal in “secret” proceedings, led by then-Treasury Secretary John Snow. These proceedings provided no justification for the deal’s approval. Members of Congress were also irate that the DP World deal had been given government approval. One notable example came from Thomas Kean, the former governor of New Jersey, who had co-led the 9/11 commission. Kean told The Times of New Jersey that the deal “shouldn’t have happened” because there was “no question that two of the 9/11 hijackers came from there and money was laundered through there.” He added, “From our point of view, we don’t want foreigners controlling our ports.” Kean’s views were echoed by then-Congressman from New York, Peter King, who said that Kean “knows as much as anyone how risky it is to deal with the United Arab Emirates. This just proves that no real investigation [into DP World] was ever conducted” as part of the deal. The UAE responded by hiring a high-powered team of lobbyists, led by former Senator Bob Dole, to salvage the deal.

It turns out that no investigations into DP World or the deal were made by the Bush administration at all. In fact, major figures in the administration had told DP World and its head, Sultan bin Sulayem, that no U.S. government investigation of the deal was required, waiving it entirely. Lawsuits filed afterward alleged that this was not true and in violation of a statute requiring that such an investigation occur when ownership of a company by a foreign government-controlled entity could impact U.S. national security. The figures in the Bush administration who had waived an investigation included Secretary of the Treasury John Snow, DHS Secretary Michael Chertoff, Secretary of State Condoleezza Rice, Secretary of Defense Donald Rumsfeld, and Attorney General Alberto Gonzales. All were members of the Committee on Foreign Investments in the United States at the time.

Reports soon appeared noting that Snow, before joining the Treasury Department in February 2003, had been the CEO of CSX, a company that had sold its international ports business to DPW a year after Snow joined the Bush administration and roughly a year or so before Snow “secretly” led the approval of DPW’s acquisition of P&O ports. The Bush administration claimed that Snow had not been personally involved in the CSX port sale to DPW in 2004, even though Snow was still receiving pension payments from the company as well as $8 million in deferred compensation from CSX the year of the deal’s approval. It was also noted that, prior to being given the top job at the Treasury, Snow had overseen the beginnings of the sale of another major CSX subsidiary to the Carlyle Group, which boasted deep ties to George Bush Sr., former Secretary of State James Baker (an Epstein associate from at least 1992 if not earlier), and the bin Laden family. The sale was formally cemented in late 2004 when Snow was the secretary of the treasury. Snow currently works for Cerberus Capital Management, whose long-time head, Steve Feinberg, is currently the deputy secretary of war in the second Trump administration.

Furthermore, a former top CSX executive who had worked under Snow, David Sanborn, had joined DPW as director of operations for Europe and Latin America. A month before the controversy around the DPW acquisition of P&O reached a boiling point, in January 2006, Sanborn was appointed to run the Maritime Administration of the Department of Transportation. The Bush administration claimed Sanborn had been nominated, not because of his ties to CSX and DPW, but because of his “experience and expertise.”

In addition to the apparent conflict of interest related to John Snow’s CSX connections, the UAE had given the Bush administration $100 million, ostensibly for Hurricane Katrina relief, not long before the deal was approved. However, the State Department denied any connection between the two events, despite the unusual timing and the fact that the UAE’s donation was several times larger than that of any other nation. Notably, billions in Katrina relief funds were wasted (and potentially looted) by federal agencies and contractors.

Concerns about these conflicts of interest further intensified when President Bush threatened to veto any law passed by Congress aimed at blocking DP World’s acquisition of the U.S. ports in question. When Congress garnered enough votes to thwart a potential presidential veto, DP World sold off its U.S. assets to American International Group (AIG) for an undisclosed sum. As noted in One Nation Under Blackmail, AIG was interwoven into a complex web of organized crime and dark money networks that were connected to the Iran-Contra affair and also boasted ties to the Bush family. In addition, AIG’s chairman at the time, Hank Greenberg, had longstanding ties to the CIA, even nearly leading it under Ronald Reagan. Greenberg also served alongside Jeffrey Epstein at the Council on Foreign Relations (CFR) and the Trilateral Commission during this period.

An Emirati Link to the Sweetheart Deal?

As previously mentioned, Bush’s Attorney General Alberto Gonzales had been part of the group of top Bush officials who had waived an investigation into the DPW deal. Notably, according to journalist Nick Bryant, either Gonzales or former President Bush was responsible for telling former U.S. Attorney Alex Acosta to “stand down” with respect to prosecuting Epstein after his first arrest in 2007. The ultimate result of this decision to “stand down” was the affirmation of Epstein’s notorious “sweetheart deal.” Congress subpoenaed Gonzales in August of last year to testify as part of the investigation into Epstein’s activities. Gonzales, however, did not testify, instead offering a sworn statement that appears not to have been made public.

It is worth considering that part of Gonzales’ or Bush’s reasoning in pressuring Acosta may have been the same rationale they both tried to force through the DP World deal. Indeed, there is a possibility that the two events are connected, as Epstein may have played a role in brokering the “secret” approval of the DP World deal. For instance, during the same time the DPW deal was taking shape in 2005, Farkas and bin Sulayem were photographed sitting in the front row of the Victoria’s Secret fashion show with Jeffrey Epstein. The lingerie brand’s owner and Epstein’s long-time benefactor, Leslie Wexner, was also in the front row. That fashion show took place on November 9, 2005. Notably, bin Sulayem’s DP World had made contact with the Bush administration about his intentions to acquire P&O’s U.S. ports a month prior, and negotiations were well underway.

Were bin Sulayem and Farkas meeting with Epstein about bin Sulayem’s most pressing issue in the United States at the time –– the DP World deal? It seems highly likely that it was brought up, if not the main reason behind their meeting. Epstein would have been capable of influencing these events to some degree –– he already boasted ties to former President Clinton and influential officials from the previous Clinton administration; he was well-connected to influential Israeli politicians who had a track record of pressuring U.S. presidential decision-making (e.g., Ehud Barak’s role in securing the presidential pardon of Marc Rich); he had long-standing and extensive ties to dark money networks connecting the Gulf nations (including the UAE) to the dark underbelly of the U.S. national security state, which –– again –– boasted ties to the Bush family.

It is also worth noting that Epstein was closely connected to key figures at the Carlyle Group during this period, which had close ties to CSX, the UAE, and the Bush family simultaneously. Carlyle has, notably, long been regarded as “the CIA of the business world – omnipresent, powerful, a little sinister,” as the Washington Post once stated.

Epstein was a member of the Rockefeller-created Trilateral Commission when David Rubenstein, co-founder of the Carlyle Group, joined the organization. They also served together on the Council of Foreign Relations (CFR). Epstein likely gained membership in these organizations through his apparent association with the Rockefellers, as claims that he managed “Rockefeller money” had circulated in the press well before his first arrest in the mid-2000s (Epstein also sat on the board of Rockefeller University during that period).

Rubenstein was also connected to Epstein’s financial network, sitting on the National Advisory Committee of JP Morgan, which –– at the time –– was intimately connected to the Wexner family’s interests as well as Epstein’s USVI activities, including those that intersected with Andrew Farkas (discussed in detail in a subsequent part of this article). However, the clearest ties emerge from the close relationship between Rubenstein’s wife from 1983 to 2017, Alice Rogoff, and Ghislaine Maxwell, along with organizations tied to Maxwell (e.g., TerraMar), and Maxwell’s “secret” husband Scott Borgerson.

However, another figure at Carlyle Group who was arguably closer to Epstein was former Secretary of State James Baker. Baker worked for Carlyle from 1993 until his retirement in 2005, during which time he helped expand Carlyle overseas, including into the UAE. Prior to that, he was secretary of state under the administration of George Bush Sr. Baker had an established yet murky relationship with Jeffrey Epstein, as confirmed by Epstein’s lawyer Jeffrey Schantz. Epstein’s relationship with Baker, as revealed in documents related to later litigation between the State Department and Epstein, enabled Epstein to lease a large State Department property in Manhattan, beginning in 1992, while Baker was still serving as secretary of state until 1997. Connections between Epstein and top figures at the Bush-linked Carlyle Group suggest another possible reason the Bush administration intervened in Epstein’s 2007 court case, as detailed above.

Reporting from Drop Site News last year revealed that bin Sulayem worked to arrange a meeting with Epstein in November 2006, roughly a year after they were pictured together at the Victoria’s Secret fashion show with Farkas. Drop Site notes that the email correspondence between the two men was in the aftermath of the DP World scandal and that Epstein was eager to meet Sultan bin Sulayem, urging him to “come sooner.” The article also notes that in the following year, which saw Epstein’s first arrest and the Bush administration’s intervention to broker the “sweetheart deal,” Epstein advised bin Sulayem on an expected IPO for DP World and reviewed the then-unpublished book manuscript of Dubai’s ruler, Mohammed bin Rashid al-Maktoum. Also, in a few 2007 emails, the two men crudely discussed women, business strategy, and arranged vacations on Epstein’s private island. In a March 2007 email to bin Sulayem cited by Drop Site News, Epstein told him that he had “the three largest private equity people in the states,, [sic] excited about visiting dubai” and asked about “boat plans” and if they could “go to turkey” together in April 2007. It seems almost certain that one of the “largest private equity people” in the United States Epstein referenced was David Rubenstein or another top executive at the private equity giant, the Carlyle Group. This is especially likely given Rubenstein’s and Carlyle’s connections to Epstein, noted earlier in this article.

Notably, a few months after Epstein sent this email to bin Sulayem, Carlyle announced in September 2007 that it would sell a 7.5% stake in its operations, worth $1.4 billion, to an investment arm of the UAE government, specifically Mubadala. Mubadala had also committed $500 million to an investment fund Carlyle managed as part of the deal, under an agreement brokered earlier that year by Carlyle executives and UAE officials. One of the Carlyle executives in question was Rubenstein. This exchange again lends further credence to the possibility that connections between Epstein, the UAE, and Bush-connected firms like Carlyle influenced the Bush administration’s handling of the 2007 criminal case against Epstein.

Another interesting wrinkle is that as Carlyle (and Rubenstein) embarked on a trip to Dubai, apparently with Epstein’s direct involvement, Dubai Aerospace made a deal to purchase Landmark Aviation from the Carlyle Group in August 2007 as part of a $1.9 billion agreement. Notably, Landmark Aviation had, by that point, been involved in extraordinary rendition flights on behalf of the CIA. Its board also included figures such as former CIA head James Schlesinger and former Pentagon comptroller Dov Zakheim. Landmark Aviation, along with the Epstein-connected Lane Aviation, was one of the two private terminal operators at Port Columbus in Ohio at Rickenbacker airport. They took over that role from the CIA-linked airline Southern Air Transport, which had moved to Rickenbacker because of lobbying efforts closely tied to Leslie Wexner and Jeffrey Epstein.

As noted in One Nation Under Blackmail, 2011 lobbying efforts linked to Wexner led to rule changes that allowed U.S. customs officials to clear private planes at the private terminals controlled by Lane and Landmark instead of the main terminal. Given that Rickenbacker airport, particularly from the Southern Air Transport era and onward, was suspected of smuggling and links to organized crime, including by Ohio state officials, Wexner-led legal efforts suggest that the CIA contractor Landmark Aviation was potentially involved in these activities. As in the case of DP World and U.S. ports, there was government resistance to a Dubai-based company taking over the management of these private terminals, which eventually forced Dubai Aerospace to sell off some of Landmark’s U.S.-based assets. The Carlyle Group then moved to reacquire Landmark in 2012 for an undisclosed sum.

It is also worth noting that Epstein, as well as the broader network of intelligence and criminal interests he served, would have been interested in developing close ties to DP World and extending its network into the United States due to his history in arms trafficking and smuggling networks. Indeed, Epstein had a reputation for smuggling weapons in the 1980s into the 1990s, overlapping with his aforementioned involvement in the relocation of the CIA-linked Southern Air Transport on Wexner’s behalf in the mid-1990s. During much of this period, he was linked to BCCI, the CIA-linked bank used by intelligence agencies, mobsters, and drug cartels. Among its many financial crimes, the bank also engaged in a sex trafficking operation where pre-pubescent girls were trafficked to UAE elites who were “VIPs” of the bank. The sex trafficking operation, as described in the U.S. Senate report on BCCI, bears remarkable similarities to the sex trafficking operation in which Epstein and Ghislaine Maxwell would later engage.

Epstein’s known ties to Gulf countries, notably Saudi Arabia, were first forged during this period, as evidenced by the travel stamps on Epstein’s Austrian passport discovered during the 2019 raid on his New York residence. Drop Site notably details how, during the 1980s, when BCCI and the UAE were at their closest, bin Sulayem became the chairman of the Jebel Ali Free Zone Association. This group controlled Dubai’s largest “free trade” port, which –– as the authors note –– did not report cargo data to the United Nations and allowed firms to move cargo by boat or plane without customs inspections. The result under bin Sulayem’s watch was that “free zones” in the UAE like those bin Sulayem managed (he later led the Dubai Port Authority) became “popular transit points for illicit goods traveling to and from Africa.» Many of the goods smuggled through UAE ports under bin Sulayem were the very “arms, drugs and diamonds” that Epstein previously bragged to journalist Vicky Ward as having allowed him to amass a fortune.

From Dubai World to Debt World

Yet another layer of connective tissue fleshing out the Epstein–bin Sulayem–Farkas connections can be found during this period. This particular connection involves the 2008 financial crisis and how it brought Dubai World to the brink, largely due to the activities of Farkas and Epstein-linked bankers, and potentially, Epstein himself.

In 2003, Farkas helped create the Emirates National Securitisation Company (ENSeC), which was “created specifically to facilitate the development of a secondary mortgage system in Dubai, similar to Fannie Mae and Freddie Mac in the United States.” Initially, a partnership of Dubai Islamic Bank, the bin Sulayem-controlled Istithmar, Bahamas-based Pender Ltd., and Farkas’ Island Capital, ENSeC issued commercial mortgage-backed securities to “create adequate liquidity in the mortgage financing for the real estate sector.” Farkas served as its executive vice chairman. Later reports credited Farkas with “help[ing] Dubai set up a Sharia-compliant mortgage industry.”

One report from May 2005 revealed that a considerable amount of ENSeC’s activities were conducted by ENSeC Home Financial Pool I Ltd., a Cayman Islands-registered special purpose vehicle (SPV). The report also noted that, in 2005, this Cayman-linked entity issued $350 million in bonds linked to $350 million in mortgages for properties at The Palm, Jumeirah. Per the report, demand for the bonds exceeded $4 billion. The use of the Cayman Islands here is interesting, given that these islands, as well as other Caribbean offshore tax havens, were used by major banks in the lead-up to the 2008 financial crisis to move toxic mortgage assets off their balance sheets by parking mortgage-backed securities with Cayman Islands financial institutions.

Soon after its launch, Bear Stearns and Citigroup also became involved with ENSeC as placement agents. ENSeC was created in 2004 in the lead-up to the global financial crisis in 2008, largely driven by the explosion of mortgage-backed securities. At the time, Epstein was closely linked to Bear Stearns, particularly Bear Stearns’ toxic mortgage-backed securities. At the time, Citigroup was chaired by Robert Rubin, the former Treasury Secretary who helped deregulate the banking sector, thereby helping create the 2008 economic crisis. Rubin was also the official at the Clinton White House who is believed to have first invited Epstein to the president’s official residence in 1993, and his deputy and later successor, Larry Summers, was courted by Epstein and flew on Epstein’s private plane while serving in the Treasury’s top post. During that period, Summers oversaw the repeal of the Glass-Steagall Act, creating the modern Citigroup, and laid the groundwork for the subsequent 2008 crisis. In recently released emails, Summers refers to his close friend Jeffrey Epstein as «Mr. Money.»

Epstein was directly involved with toxic and risky mortgage-backed securities as chairman of the $6.7 billion company Liquid Funding from 2001 until at least March 2007. Bear Stearns, Epstein’s former employer, had a 40% stake in Liquid Funding. It is unknown whether any of the mortgage-backed securities created by the Farkas-linked ENSeC ended up being held by Liquid Funding, but given the connections between Epstein, Farkas, bin Sulayem, ENSeC, and Bear Stearns, it seems likely. This is even more likely given that Epstein was pictured with Farkas and bin Sulayem shortly after ENSeC was created, as well as Epstein’s known ties to bin Sulayem and the UAE after 2005 — not to mention the fact that Epstein was considered a foremost expert in the exact type of financing in which ENSeC, Bear Stearns, and others were involved. For instance, Epstein was infamously described as the inventor of derivatives by figures like Reid Hoffman. As a result, it is possibile that Epstein had advised Farkas and bin Sulayem about ENSeC in the lead-up to the 2008 crisis. Adding to this possibility is a recent Bloomberg report, which revealed that Epstein had at least one bank account in the Cayman Islands that were reportedly linked to criminal activity.

In addition, after Dubai World suffered from bad debt due to its links to ENSeC and the global economic crisis, Epstein attempted to find the struggling company a buyer. More specifically, Epstein tried to convince Jes Staley to market Dubai World to the Chinese in 2009. In November of that year, Staley forwarded Epstein an internal email regarding high-level talks with senior officials from the Dubai and Abu Dhabi departments of finance. A few days later, Epstein subsequently wrote to Staley, “The first most elegant deal that you can do. is to have China buy Dubai World Ports. They want turnkey, ops where they can then use their worldwide construction cos for building. would be a first great deal for the new ceo of the IB [investment bank].” Furthermore, in December 2009, Epstein attempted to schedule a meeting between bin Sulyaman and Staley. Epstein told Staley that “sultan is laying the groundwork for you to establish a serious presence. Jpm [JP Morgan] reputation in the region is poor.”

Dubai World’s debt crisis was truly massive, so much so that it threatened the UAE’s entire economy. After investors panicked and the country’s economy teetered, Dubai World attempted to calm them by stating that only its real estate developer, Nakheel, which had been intimately involved with ENSeC, was in peril. Reports noted that Rothschild banking interests, which Epstein was known to represent, were advising the debt restructuring efforts. Dubai World was set to default on December 14th, 2009, but disaster was averted that very morning by a $10 billion bailout from the UAE government that very morning. It seems almost certain, given the timing of his emails, that Epstein was attempting to use Staley and his bank, JP Morgan, to find a buyer to fix the serious problems that Farkas, and likely Epstein, appear to have created for Nakheel and its parent company, Dubai World.

To tie these worlds even closer together, consider Unlimited Hangout’s previous reporting detailing the close ties of Leslie Wexner and other Wexner-linked figures to JP Morgan, which notably swallowed up Bear Stearns after the 2008 financial crisis, and its current CEO, Jamie Dimon. Shortly thereafter, JP Morgan became a major facilitator of Epstein’s financial crimes and sex trafficking operations, per a lawsuit filed against the bank by the U.S. Virgin Islands, with JP Morgan paying $75 million to settle the case out of court in 2023.

Notably, none of the financial troubles he had helped create for Dubai World ended up hurting Andrew Farkas. As noted by the Observer:

Before Dubai World revealed its debt troubles, Mr. Farkas sold his [Dubai World-linked] marina interests to a Qatari firm, relinquished his interests in ENSeC, and sold his equity stakes in all of his Dubai World joint ventures in New York, save perhaps the most valuable, the Mandarin Oriental hotel in the Time Warner Center.

Somehow, Farkas knew exactly when it was time to get out. This seems to be a recurring pattern for him.

Yacht Havens, Tax Havens

Soon after Andrew Farkas founded Island Capital, he became intimately involved in the development of marinas both in Dubai and elsewhere. The company soon created a subsidiary called Island Global Yachting (IGY) in the USVI in 2005. Yet, before IGY was formally created, Farkas’ first marina project, the Yacht Haven Grande in Saint Thomas, USVI, began construction in 2004 and opened in 2007. The project’s acquisition allegedly dates back to 2001, years before Farkas founded Island Capital. In fact, in June 2003, the Yacht Haven properties were still owned by Farkas’ Insignia before being transferred to “CEO Andrew Farkas’s Island Fund I LLC,” an apparent precursor to Island Capital.

Andrew Farkas acquired another USVI harbor, American Yacht Harbor, in January 2007 for an undisclosed sum. Farkas gave half of the marina’s ownership to Jeffrey Epstein. It is also unknown how much Epstein paid, if anything, for his stake in the marina. Epstein had developed a presence in the USVI long before, purchasing Little Saint James island in 1998 for an estimated $8 million. However, as recently released emails reveal, Epstein and Farkas planned the acquisition of American Yacht Harbor together, despite Farkas previously denying it.

Having already established that Farkas and Epstein knew each other by November 2005, the reality is that the two men likely became acquainted earlier, given that Farkas’ own uncle, Jonathan Farkas, met Epstein during the 1982 recession and became a long-time friend. Jonathan Farkas later claimed that he was enthralled by Epstein upon meeting him, particularly by his “absolute certainty that he knew where the economy was going.” Jonathan remained close to Epstein from that time on, as evidenced by him infamously begging Epstein in 2017 to tell him if his mistress was “a hooker.” A few years earlier, Jonathan Farkas had also admitted to visiting Epstein when he was under house arrest following his first legal case involving minors. As will be noted shortly, Andrew Farkas also visited Epstein regularly during this period.

Jonathan Farkas’ wife, Somers Farkas, was also fond of Epstein, stating in a 2010 email, “I do know Jeffrey, and I like him. You wouldn’t think I would, but I do.” Somers Farkas is currently serving as U.S. ambassador to Malta and was appointed to the position by Trump after she donated $300,000 to his campaign. Oddly, her mother-in-law, Ruth Farkas, had paid the same sum to the 1972 Nixon campaign decades earlier. Testimony from the Watergate hearings revealed that she knew the money would result in her receiving an ambassadorship. Aside from Jonathan Farkas, another possibility for who may have first connected Farkas and Epstein is Donald Trump, who knew both men well prior to 2005. However, during the 1990s, both Epstein and Farkas were deeply involved in New York real estate, particularly “distressed” properties, which may have led them to meet through those avenues.

A month after Farkas and bin Sulayem joined Epstein at the Victoria’s Secret annual fashion show, in December 2005, Farkas’ IGY partnered with Dubai World’s Nakheel “to design, develop and manage all of Nakheel’s marina properties in Dubai.” Another Dubai World subsidiary, Istithmar, announced that it held around 25% equity in Island Global Yachting’s projects in Dubai and Saint Thomas, USVI. Farkas subsequently became heavily involved in even more UAE marinas, and IGY expanded by acquiring marinas in various countries. IGY’s holdings in the Caribbean grew rapidly after it acquired Sun Resorts International, which had belonged to the Kerzner family. As previously mentioned, the Kerzners were the controversial hotel dynasty that had brokered Farkas’ introduction to bin Sulayem in 2002.

Roughly a year later, in November 2006, Farkas emailed Epstein to tell him, “We are now in contract to buy American Yacht Harbor, where you keep your tenders.” At the time, Epstein already had some of his businesses registered at the marina. Epstein responded, “I would like to be in on that.” Epstein likely wanted to be “in on that” not only because he had businesses registered in that location, but also because he had paid $1.2 million in 2004 for the laying of a massive underwater fiber-optic cable from near American Yacht Harbor in Red Hook to his private island, Little Saint James.

Not long after IGY acquired the marina, its other USVI marina, Yacht Haven Grande, was in major financial trouble and nearly went bankrupt until IGY acquired the marina’s $120 million in debt in September 2008. Roughly a year later, in December 2009, Epstein claimed in an email to banker Jes Staley that he “owned” both American Yacht Harbor and Yacht Haven Grande. No evidence has been provided formally linking Epstein to Yacht Haven Grande. However, Epstein may have claimed ownership because he could influence the use of its facilities through his close relationship with Andrew Farkas. The relationship was indeed close, as new emails reveal, with Farkas regularly visiting Epstein during his 13-month jail sentence between 2008 and 2009. Though Farkas’ name did not appear on any visitor log, the New York Times recently reported that Farkas would meet his “dear friend” Epstein during the day, when Epstein was allowed to go to his Palm Beach office for a 12-hour “workday.”

In 2009, after his release from prison, Epstein changed his primary residence to his private island in the USVI. From then on, Farkas and Epstein regularly applied and then reapplied for special tax breaks with the Virgin Islands government, specifically its Economic Development Authority. The Times highlighted one email exchange where Farkas told Epstein in August 2009, “IGY finance and tax guy are going to speak with your guys to reconcile the tax treatment for you.” Epstein garnered an estimated $300 million in tax incentives from this point up until near his 2019 arrest. It is unclear how much Farkas financially benefited over that same timeline, given that their tax breaks were often coordinated.

A likely reason Epstein changed his primary residence to the USVI during this time is that he anticipated enjoying other special privileges there that went far beyond tax breaks. That was because the USVI’s governor, beginning in 2007, was John De Jongh, and Epstein had employed De Jongh’s wife, Cecile, since at least the year 2000. Cecile officially worked as an office manager for Epstein’s Financial Trust Company and later Southern Trust Company, both headquartered at American Yacht Harbor (co-owned by Farkas and Epstein since 2007). Over the course of De Jongh’s time in office, the political, economic, and other favors that he and his wife paid to Epstein were considerable.

For instance, it was later reported that Cecile De Jongh had helped Epstein obtain student visas for young women who were visiting the island under dubious circumstances while her husband was in office. This occurred the same year Epstein donated around $20,000 to the university that was named in connection with the visas. She also helped manage, and often seemed to direct, Epstein’s donations to USVI politicians while also helping influence the passage of legislation that helped Epstein waive a lot of the requirements he was expected to follow as a registered sex offender, especially with respect to his whereabouts and travel.

Another notable example of Cecile’s role as a conduit for Epstein’s political donations concerns Celestino White Sr., a longtime USVI Senator who helped oversee the USVI airport where Epstein also enjoyed special privileges (more on that shortly). As the Miami Herald reported in 2023:

Emails included in the [USVI vs. JP Morgan] lawsuit discovery show that White’s ‘consulting and management firm’ sent Epstein a contract for unexplained services for his island. ‘Senator White signed the contractor’s agreement and the confidentiality agreement …we will need to get him a check for $10,000 by Friday,’ Cecile de Jongh wrote to Epstein. ‘Approved.’ Epstein wrote back. In 2015, Cecile de Jongh suggested to Epstein: ‘You may want to consider putting Celestino on some sort of monthly retainer. That is what will get you his loyalty and access.’