Shayne Coplan, now the world’s youngest “self-made” billionaire, is the public face of what purports to be the world’s largest crypto-powered prediction market – Polymarket. Coplan and his alleged arch-rival, Tarek Mansour of the competing prediction market platform Kalshi, recently buried the hatchet to create a new venture capital firm called 5c(c) Capital, a reference to the section of the Commodity Exchange Act which is currently used to regulate prediction markets. The fund is aimed at bulking up the infrastructure for what has rapidly become an insurgent digital industry.

Since the early days of Donald Trump’s 2nd term, prediction markets like Polymarket and Kalshi have largely been told to police themselves. This comes courtesy of the current head of the (CFTC), Michael Selig, who was previously a lawyer representing major cryptocurrency industry clients. Selig became the CFTC chair only after the Trump administration rescinded the nomination of Brain Quintenz, who then sat on Kalshi’s board and worked for the crypto venture team at Marc Andreessen’s firm Andreessen Horowitz. Andreessen Horowitz has notably backed Coplan’s new prediction market VC firm 5c(c) Capital and is also heavily invested in Kalshi.

During the past couple of years, Polymarket and Kalshi have become important components of reporting on global finance and politics. This is partially due to their extensive cultivation of wide-ranging media partnerships. For instance, in the case of Polymarket, the company now boast partnerships with the Wall Street Journal and its parent company Dow Jones, as well as Yahoo! Finance, Substack and the live-streaming platform Parti. While these partnerships have been framed as an effort to further legitimize prediction markets, concerns have been raised that these media partnerships could be used to intentionally manipulate these very markets via the implantation of false and misleading stories.

Concerns like these have dogged these new prediction markets just as their star has risen. Insider trading allegations, including from the platforms themselves, have shown how prediction markets can be abused by traders with insider access to market movers and policy makers. Now with Congress trying to get involved, both Polymarket and Kalshi have announced new efforts to work to improve “market integrity” without the need for government intervention. However, the effects of their efforts remain to be seen, as several of the new measures are based on traders self-reporting their conflicts of interests.

Concerns about widespread insider trading have only been exacerbated by both the White House’s open dismissal of those concerns as well as the Trump family’s close ties to both Polymarket and Kalshi. For instance, Trump’s son, Donald Trump Jr., is both a strategic advisor to Kalshi and also advises Polymarket. Trump Jr. is also a major investor in Polymarket via his venture capital firm 1789 Capital. The evidence of insider trading on these platforms, particularly in cases where it is directly related to Trump’s “most consequential decisions,” is now widely acknowledged by mainstream media.

While the ascendance, and arguably the normalization, of insider trading are being treated as unintended “flukes” of these markets, there is an argument to be made that they are operating just as intended. Some of the evidence for that argument can be found in what appears to be Polymarket’s true origins.

Despite being nominally founded in 2020, Coplan –– in founding his company –– was admittedly following the model of the Big Tech billionaires he had admired as a teen, particularly those who created their flagship companies by rebranding and privatizing controversial military programs from the George W. Bush era for maximum profit and, seemingly, to advance even darker ambitions.

Previous reports from Unlimited Hangout have explored how Mark Zuckerberg’s Facebook gave new life to the Pentagon’s LifeLog program the day it was shut down and how Peter Thiel’s Palantir was created as a privatized version of the Pentagon’s surveillance dragnet program Total Information Awareness. In this two-part series, we now examine how Shayne Coplan appears to have rebranded and privatized yet another failed Pentagon program from that same era.

By following in the footsteps of his admitted idol, Zuckerberg, and backed by funding from Thiel-linked sources, Coplan has managed to resurrect the Policy Analysis Market (PAM), one of the most controversial Pentagon programs from its now defunct Information Awareness Office (IAO). Tellingly, his efforts to launch Polymarket included direct communication with one of the main architects of the PAM program and he was also greatly influenced by another apparent Thiel-linked effort to resurrect PAM that failed.

Importantly, Coplan’s apparent re-brand of PAM –– often referred to in the past as the “Terrorism Futures Market” ––is about more than just reaping mega-profits in an era where insider trading and financial corruption are flourishing with the White House’s blessing. As will be explored in Part II of this series, an ulterior motive directly linked to Coplan’s efforts aims to advance an extremely dystopian governance model that is of great interest to the Big Tech billionaires now closely linked to Coplan and the dominant prediction market companies, such as Peter Thiel and Marc Andreessen.

A Brief History of American Prediction Markets

The story of prediction markets began in the late 1980s, when a handful of professors teaching at the University of Iowa created what they initially called the Iowa Political Stock Market. As part of their market experiment, university staff and students were recruited to trade contracts on the 1988 U.S. presidential election between George H.W. Bush and his Democratic challenger Michael Dukakis. It quickly became a popular phenomenon in the finance and accounting departments of the University of Iowa, and later expanded far beyond its halls. Under the name of the Iowa Electronics Market or IEM, it soon became open to anyone who wanted to open an account, so long as they completed a one-page application and sent the market operators a check in the mail. By the time the next presidential election took place in 1992, the IEM had received an exemption from the Commodity Futures Trading Commission (CFTC), allowing it to operate without regulation so long as it was run for “solely academic and experimental purposes,” did not use outside advertising, and individual traders were prohibited from investing more than $500.

The premise of the experiment that later became the IEM was that, while voters have no incentive to be honest with pollsters, they would respond to information differently if their own money was on the line. “There is a strong incentive for players in these political markets to process information about the candidates and their conclusions are revealed to us through the markets’ prices,” the Wall Street Journal quoted Steven Feinstein, then an assistant professor of finance at Boston University’s School of Management, as saying. The Wall Street Journal, writing on the IEM in 1995, also noted that one of the ways in which the IEM was particularly useful was because “shareholders can react quickly to developments.” The article also quotes Sheryl Ball, formerly an assistant professor of economics at Virginia Polytechnic Institute and State University, as saying “by watching the political stock market it is possible to gauge the effect of an ad, a policy announcement or an alleged affair on the part of a candidate almost instantaneously.” The idea of using prediction markets as an important indicator of how the public will react to a given piece of information would later serve as a foundational concept for “futarchy” – to be discussed in detail in Part II – which proposes using prediction markets as a new system of public governance.

After the popularity of the IEM, another iteration of the prediction market was launched in 1994 by Mark James, Sean Morgan and Robin Hanson. Robin Hanson was a researcher into Artificial Intelligence, Bayesian statistics and other topics for military contractor Lockheed as well as NASA in the late 1980s and early 1990s, and is also credited with creating the concept of “idea futures” after being inspired by IEM’s success. Per Hanson, “idea futures” would see the harnessing of market principles to “predict a wide range of political, social and technological outcomes.” Hanson has also claimed to have led the development of the first internal, corporate prediction market in 1990 for Xanadu Inc.

Despite what he lists on his CV, it appears that Hanson did a significant amount of his work for NASA, not as a direct employee, but rather as a contractor via the private company Sterling Software. Hanson does not publicly list his past employment with Sterling on his CV, but his publications from this period reveal his status as a Sterling employee while it contracted for NASA.

Sterling Software was largely run by Dallas-based billionaires Sam Wyly and his brother Charles. The Wyly brothers were closely associated with the political fortunes of George W. Bush, counting among his largest political donors from his gubernatorial campaigns and into his presidential runs. The Wylys obtained the NASA contracts, on which Hanson worked, through Sterling’s controversial acquisition of Informatics General Corporation in 1985. Sterling’s de facto hostile takeover of Informatics was made possible by the criminal bank Drexel Burnham Lambert, which was closely tied to the Savings and Loans crisis of that era and criminal activities tied to both intelligence agencies and the Bush family. Notably, during the Drexel-backed efforts of the Wylys to seize control of Informatics, Charles Hurwitz, the mob-adjacent corporate raider with significant ties to the most notorious actors of the Savings and Loans crisis, took a 13.3% stake in the company to facilitate Sterling Software’s takeover. While Hanson was merely employed by Sterling a few years after the Informatics takeover, it is worth noting that he would later help the Pentagon design what is arguably the most controversial prediction market of all time during George W. Bush’s presidency and would also later greatly influence Elon Musk, the brother of Sam Wyly’s son-in-law Kimbal Musk. The Musk-Hanson relationship is discussed in Part II of this series.

After leaving (for a time) government contract work, Hanson created the Foresight Exchange in 1994. Foresight has been described as “the world’s first web-based betting market,” but managed to evade U.S. regulatory scrutiny by using play money (called “credibills”) that could be exchanged for prizes. Hanson’s co-founders of Foresight Exchange, Mark James and Sean Morgan, were employees of the Canadian government-funded Alberta Research Council (now known as Alberta Innovates). James and Morgan became interested in Hanson’s 1992 paper that outlined the concept of “idea futures” and decided to make Hanson’s ideas a reality. Hanson had written that paper as a visiting researcher for the Foresight Institute, which was founded in 1986 to promote the development of nanotechnology, Artificial General Intelligence (AGI) and longevity research. These interests would bring the Foresight Institute close to the “philanthropic” interests of tech billionaire Peter Thiel by the early 2000s and the institute has since been credited with spurring Thiel’s early interest in investing in AI companies.

While the IEM was focused largely on electoral campaigns, Hanson’s Foresight Exchange was seemingly the first iteration of the modern prediction market, whereby the outcome of any query could be bet upon. For instance, archives of Foresight’s old website show that it dealt with, not only US and UK politics, but also Religion and “New Age” phenomena; Scientific queries dealing with Medicine, Space, Physics, and the future of Computing; and issues dealing with Arts and Entertainment, such as Television and Movies.

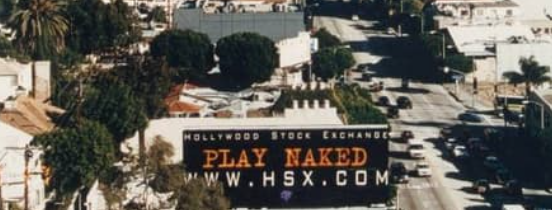

Movies were, incidentally, the focus of the world’s next prediction market, the Hollywood Stock Exchange (HSX). Founded in 1996, HSX was described by the New York Times as a “virtual stock market of fake stocks and fake money with such a fanatic following that players are offering hundreds of real dollars to buy a make-believe portfolio.” It was created by two men who were, at that point, best known as veterans of Wall Street but have since become better known for other pursuits. For instance, HSX co-founder Max Keiser went on to become best known for his early, and often eccentric, evangelism of Bitcoin, while the other co-founder, Michael Burns, is now best known for his top role at Lionsgate Films.

In 2001, the HSX, along with its critically important patents, was acquired by Cantor Fitzgerald, the American financial services firm long helmed by the current Commerce Secretary Howard Lutnick. Lutnick and Cantor had planned to do away with HSX’s “play money” and lead the push to turn speculation on movie performance into “real money” via commodity futures contracts. In other words, they sought to pioneer a “film futures” market.

Paul G. Anderson explained the concept of Cantor’s proposed film futures market as follows:

Unlike the various physical commodities that trade on futures exchanges, such as corn, oil, and wheat, the relevant commodity in a film futures contract is an intangible financial instrument–DBOR–whose final value is tied directly to the domestic box office revenue from ticket sales of the underlying motion picture. Thus, any film futures contract is an agreement to buy or sell DBORs at the agreed-upon price, regardless of its market value at the time that cash settlement is due. In this respect, film futures are akin to futures contracts for stock indexes, United States treasury bonds (“T-bonds”), and other ‘nontraditional’ commodities that are commonplace on most futures exchanges.

Cantor’s initial push for the film futures market was closely related to the efforts of the Republican-led Congress to pass the Commodity Futures Modernization Act in 2001, a law which facilitated –– among other things –– the “exotic trading instruments” that later played a significant role in the 2008 economic crisis. Roughly four months after acquiring HSX, Cantor Fitzgerald’s main location in New York City was obliterated during the 9/11 attacks, with Lutnick being among the small handful of survivors who happened to be out of office when the towers were struck. As a result of the massive loss of employees and company assets, Lutnick’s efforts to merge “play money” prediction markets with futures trading were delayed until roughly 2007, when he and Cantor began to revive their prior efforts to pursue film futures.

Lutnick hired Rich Jaycobs, a derivatives specialist, and together they mounted a Congressional charm offensive. By 2010, they had managed to get approval from the CFTC. However, due to Congressional opposition related to the 2008 economic crisis and also from the Motion Picture Association of America, their efforts were for naught. The negative mood, both in Congress and beyond, saw a clause added to the Dodd-Frank Act (a.k.a Wall Street Reform Act) that saw the domestic trading of film futures explicitly banned. While his efforts to legalize “real money” prediction markets alongside Howard Lutnick may have failed, Rich Jaycobs has since become the Head of Market Expansion for Shayne Coplan’s Polymarket.

DARPA Discovers Prediction Markets

Robin Hanson, the inventor of Idea Futures who had helped create the Foresight Exchange, got his biggest break to expand on his ideas and develop a new prediction market just a few months before Cantor Fitzgerald acquired the Hollywood Stock Exchange with the hopes of building an unconventional futures market. That break came courtesy of the U.S. Department of Defense (now the Department of War) and its sub-agency, DARPA.

Sometime in the year 2000, Michael Foster, a DARPA program manager working on quantum computer research backed by the National Science Foundation, learned of Hanson’s efforts as well as those of the IEM. Foster then “convinced colleagues at DARPA that their agency should fund research into prediction markets that could potentially be used to guide public policy decision-making.” This was notably years before Hanson “independently” developed his ideas of “futarchy,” which posits using prediction markets as a system of public governance. These ideas and their relevance today are discussed in Part II of this investigation.

DARPA was also interested in prediction markets for other reasons, as some of the agency’s managers also “believed a prediction market could serve as an aggregation mechanism capable of bypassing bureaucratic and political obstacles to information sharing” among U.S. national security agencies. This “belief” is directly related to efforts of those same national security agencies immediately after the 9/11 attacks to blame the “siloeing of information” within agencies for the supposed “failure of imagination” that allowed the attacks to occur despite the ostensible efforts of the U.S. intelligence apparatus. This is, of course, despite the copious evidence pointing to the direct involvement of intelligence agencies in the 9/11 attacks and in the efforts to stifle any meaningful investigation into those attacks. Nevertheless, the intelligence community’s own narrative, backed by intelligence-linked contractors like Oracle’s Larry Ellison, was that extensive information sharing between federal agencies and their main contractors was necessary to prevent another 9/11-style attack from occurring.

These narratives set the stage for the deployment of intelligence-linked software programs that were promoted as solving these problems, first of Christine Maxwell’s Chiliad (Christine is Ghislaine Maxwell’s sister) and followed by Peter Thiel’s Palantir. Then-CIA Chief Information Officer Alan Wade was closely connected to the origins of both Chiliad and Palantir. He had also been a close working partner of the DARPA office that would later host the surveillance program Total Information Awareness (TIA), a Palantir predecessor, as well as the DARPA-backed prediction market Hanson would help create.

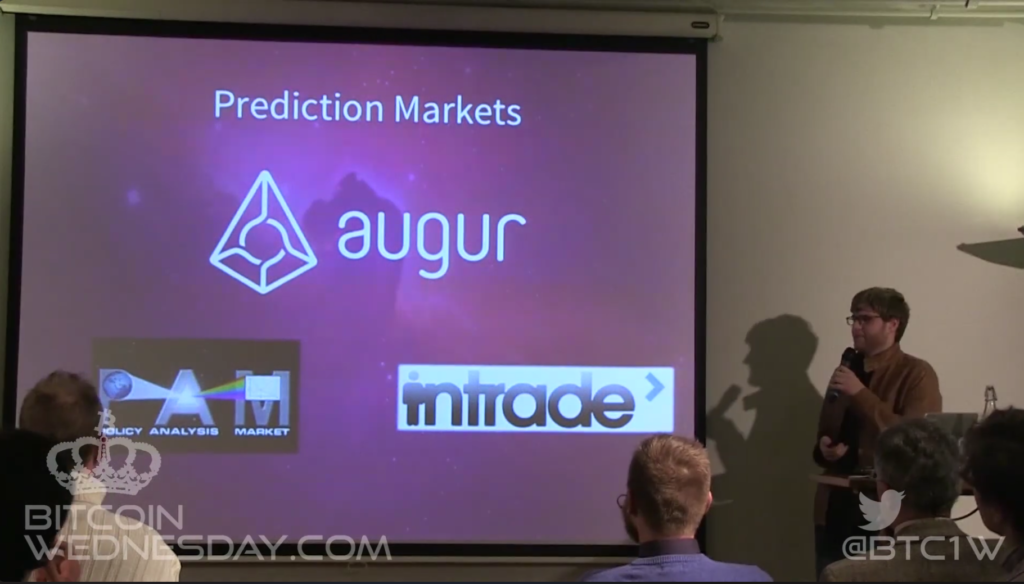

In May 2001, DARPA issued a request for proposals, one of which was called “Electronic Market-Based Decision Support.” According to an archived version of the proposal, the request sought applicants that could “design one or more markets to predict events in a limited domain of interest to the DoD” and then subsequently manage that market. Contracts related to this project were awarded to two companies, one of which was Neoteric Technologies and Net Exchange. Neoteric was a military contractor specializing in information technology and artificial intelligence, which subcontracted a company called Martek to handle this specific proposal. Martek was a private company composed largely of the architects of the IEM. Net Exchange was a company that focused on combinatorial markets, i.e. markets in which bundles of items are bought and sold, and, in applying for DARPA funding, sought to create a combinatorial prediction market. Hanson, then teaching at George Mason University, as well as another George Mason professor, David Porter, were recruited to work for Net Exchange’s program, which would later become known as the “Policy Analysis Market,” or PAM. Hanson served as the system architect for PAM. Also consulted on this project was the team of Tradesports.com/InTrade –– an Ireland-based prediction market funded by Paul Tudor Jones, Stan Druckenmiller and Rupert Murdoch. Its then-chief executive John Delaney, who later died while scaling Mount Everest in 2011, told the UK’s Evening Standard that it had additionally offered DARPA and PAM its “data, service and assistance.”

A year later, in 2002, Michael Foster’s DARPA program “Futures Markets Applied to Prediction” (FutureMAP), which had included the Hanson-affiliated PAM, was placed within a newly created office at DARPA called the Information Awareness Office (IAO). The office had been created at the behest of John Poindexter, known simultaneously for being the highest-ranking Reagan administration official convicted in relation to the Iran-Contra scandal and also for being the “godfather” of modern surveillance. Poindexter was subsequently hired as a DARPA executive and put in charge of the new office he had lobbied for, IAO. IAO’s flagship program, Total Information Awareness (TIA) –– an unprecedented surveillance dragnet that sought to develop predictive applications for national security and law enforcement similar to “pre-crime” –– was also Poindexter’s brainchild. The IAO also housed various projects aside from TIA, such as Foster’s FutureMAP program, of which Hanson’s PAM was part.

Just like TIA, the goal of PAM and FutureMAP at large was “avoiding surprise and predicting future events.” Whereas TIA sought to predict terrorist and criminal activity before it could occur through mass surveillance of Americans’ daily activities, PAM focused on using “market-based techniques” for similar ends. However, in the case of PAM, its efforts to predict events included, but went far beyond terrorist activity. PAM also sought to focus on global and regional political stability, predicting the timing and impact of emerging technologies, predicting the outcomes of advanced technology and “other future events of interest to the DoD.” Hanson has noted that other areas of interests had also included “growth rates or oil prices.”

TIA and PAM, along with the vast majority of the programs housed within the IAO, were intended to interface. Put differently, PAM and other IAO programs were created with the intention of being directly connected to TIA and to each other in order to improve the accuracy of predictions. This is even reflected in the logos of PAM and TIA. The IAO/TIA logo, which has since become infamous, shows a one-eyed pyramid surveilling the entire Earth, flanked by the phrase “science is power” in Latin. The PAM logo places the pyramid within the letter A and that pyramid, like the TIA pyramid, is also surveilling the Earth, while also shooting out a beam from its opposite side that touches a market graph.

PAM involved not only Hanson and the DARPA contractor that employed him, NetExchange, but also intimately involved The Economist magazine’s Economists Intelligence Unit (EIU). Though most know The Economist for its media publications, the EIU offers its services to businesses and governments and provides them with forecasting and advisory services. They offer, among other services, reports on the economic, political and business environments in 205 countries to help their clients “understand how the world is changing and how that creates opportunities to be seized and risks to be managed.”

According to the now archived PAM website: “The Economist Intelligence Unit is working with Net Exchange to collect and process the data on which the securities in PAM are based, and then to assess the value of the securities when they mature.”

Coincidentally, around the time that the EIU was becoming involved with DARPA and PAM, Lynn Forester de Rothschild and her husband Evelyn de Rothschild –– who boasted close ties to figures like Henry Kissinger, Jeffrey Epstein and the Clintons –– sought a significant 26.9% stake in The Economist parent company, which was finalized in 2003.

Reportedly due to the high cost of the EIU’s services per country, the designers of PAM decided to focus on eight Middle Eastern nations for their prediction market experiment: Turkey, Syria, Israel, Saudi Arabia, Iraq, Iran, Jordan and Egypt. The intention was to have select participants engage in trading activities every 3 months for a 2 year test period to determine the prices for five different parameters for each nation. These parameters included: “U.S. financial involvement in each, U.S. military activity in each, that nation’s economic growth, level of political instability, and its own military’s activities.” Traders were also expected to predict values for common economic indicators like Gross Domestic Product as well as “security indicators” such as casualties resulting from terror attacks in the West and casualties of the U.S. military. The chosen traders could also trade futures on future events that might occur within any of the eight Middle Eastern nations.

Hanson expanded on this in an article he later wrote about PAM and its efforts, stating:

[T]raders would be allowed to predict millions of combinations of the parameters, such has how moving U.S. troops out of Saudi Arabia would affect political stability there, how that would affect stability in neighboring nations, and how all that might change oil prices. Similar trades could, for example, have predicted the local and global consequences of invading Iraq, had the markets been ready then.

Initially, the goal was to have the select traders who would use PAM be employees of U.S. federal intelligence agencies. However, this became complicated by the legal barriers around “conditional transfers of funds” between federal agencies. Instead of having employees of different intelligence agencies compete, PAM then sought to recruit its traders from a single intelligence agency. However, no agency reportedly showed enough interest. As a result, they decided to open the market to select members of the public, which they were only able to do because, as agents of the DoD, they were technically exempt from anti-gambling laws.

The architects of PAM had intended to launch test operations in September 2003, with a full launch planned for January 2004. However, that timeline was interrupted when PAM became the target of significant Congressional and media criticism in July 2003, which saw PAM become publicly branded as the “Terrorism Futures Market.” The backlash against the “Terrorism Futures Market,” i.e. PAM, was arguably intensified by earlier scrutiny of the Total Information Awareness (TIA) program that, like PAM, was housed under the Poindexter-run Information Awareness Office (IAO) at DARPA.

On July 28, 2003, Senators Ron Wyden (D-OR) and Byron Dorgan (D-ND) held a joint press conference where they criticized DARPA for “spending millions of dollars on some kind of fantasy league terror game,” which they argued was “absurd and, frankly, ought to make every American angry.” Those sympathetic to PAM’s ambitions later pointed out that Wyden and Dorgan had held their press conference when DARPA’s public relations manager was “out of the office and unreachable, thus depriving that agency of a chance to offer a timely and informed response to the senators’ allegations.” A day later, the New York Times described PAM as “an online futures trading market, disclosed today by critics, in which anonymous speculators would bet on forecasting terrorist attacks, assassinations and coups.” Following the Times’ lead, a litany of negative articles quickly appeared in the nation’s press shortly thereafter and, on July 29, 2003, the Pentagon announced that it would “abandon” its plans to make PAM a reality. Public and Congressional concern over both PAM as well as TIA resulted in Congress cutting the funding for the IAO office entirely via legislation that was signed into law in September 2003.

Hanson has since expressed his views on the events that led to the shuttering of PAM and seems to regard the efforts of Wyden and Dorgan as somewhere between misguided and outright dishonest. In addition, in a 2021 interview with Richard Hanania, Hanson also expressed his view that PAM had largely failed because, two years after 9/11, people were no longer afraid enough. He stated the following about what he described as his “betting market publicity fiasco in 2003” (i.e. the shuttering of PAM):

This was soon after 9/11 and just two years later. People looked at the betting markets and said, “Oh, you’re betting on death. That’s terrible. You have to shut them down.” If they were really scared of terror attacks, if they were actually feeling a large degree of threat they would have said, “To heck with this rule against betting on death. Let’s turn on these markets. Let’s find out where the attacks are going to be so we can stop them.

Privatizing the Information Awareness Office

While it seemed that the IAO and its controversial projects had been offed by a responsive Congress, it would emerge just a few years later that TIA was never actually shut down despite being defunded by Congress. Not only were various aspects of TIA and other IAO projects “covertly divided” among U.S. military and intelligence agencies, but the core surveillance software that TIA had planned to wield began to be developed by the private company now known as Palantir, with considerable help coming from John Poindexter himself as well as the CIA’s Chief Information Officer at the time, Alan Wade. Wade had notably been one of Poindexter’s main allies and collaborators on TIA prior to its “defunding” by Congress.

In 2020, Unlimited Hangout detailed the numerous parallels between TIA and Palantir and noted the following:

At the time it was formally launched in February 2003, the TIA program was immediately controversial, leading it to change its name in May 2003 to Terrorism Information Awareness in an apparent attempt to sound less like an all-encompassing domestic surveillance system and more like a tool specifically aimed at “terrorists.” The TIA program was shuttered by the end of 2003.

The same month as the TIA name change and with a growing backlash against the program, Peter Thiel incorporated Palantir. Thiel, however, had begun creating the software behind Palantir months in advance, though he claims he can’t recall exactly when. Thiel, Karp, and other Palantir cofounders claimed for years that the company had been founded in 2004, despite the paperwork of Palantir’s incorporation by Thiel directly contradicting this claim.

Also in 2003, apparently soon after Thiel formally created Palantir, arch neocon Richard Perle called Poindexter, saying that he wanted to introduce the architect of TIA to two Silicon Valley entrepreneurs, Peter Thiel and Alex Karp. According to a report in New York Magazine, Poindexter “was precisely the person” whom Thiel and Karp wanted to meet, mainly because “their new company was similar in ambition to what Poindexter had tried to create at the Pentagon,” that is, TIA. During that meeting, Thiel and Karp sought “to pick the brain of the man now widely viewed as the godfather of modern surveillance.”

In addition to the above parallels, there is also the added fact that Palantir’s supposedly novel “selective revelation” functionality, an alleged privacy safeguard, as well as Palantir’s “immutable log” concept are not novel at all and were clearly borrowed from TIA. It is also of note that Palantir’s software stemmed from an anti-fraud algorithm called Igor, created by Thiel and Max Levchin at the company they co-founded, PayPal. In a controversial conversation with Charlie Rose in 2013, Levchin explained that “when we were working on security and anti-fraud measures at PayPal [i.e. what would become the basis for Palantir], we collaborated with every imaginable three and four-letter agency and those were some of the best, most productive relationships I’ve had as a business person.” [emphasis added]

While Poindexter’s own role in the privatization of TIA into what is now Palantir was recently noted, the CIA and its Chief Information Officer Alan Wade were also intimately involved in privatizing TIA. As Unlimited Hangout also reported:

Soon after Palantir’s incorporation, though the exact timing and details of the investment remain hidden from the public, the CIA’s In-Q-Tel became the company’s first backer, aside from Thiel himself, giving it an estimated $2 million. In-Q-Tel’s stake in Palantir would not be publicly reported until mid-2006.

The money was certainly useful. In addition, Alex Karp recently told the New York Times that “the real value of the In-Q-Tel investment was that it gave Palantir access to the CIA analysts who were its intended clients.” A key figure in the making of In-Q-Tel investments during this period, including Palantir, was the CIA’s chief information officer at the time, Alan Wade.

The CIA would continue to be intimately involved with Palantir well past this point. In fact, they became connected to such an extent that it is perfectly reasonable to argue that they are, for all intents and purposes, a CIA front company. For instance, following the In-Q-Tel investment in Palantir shortly after it was incorporated in 2003, the CIA was Palantir’s sole client until 2008 and, as Alex Karp had stated, CIA analysts were always the company’s “intended clients.” One of Palantir’s top two engineers at the time, Aki Jain, recalled making hundreds of trips to CIA headquarters between 2005 and 2009 where the CIA tested and “tweaked” Palantir’s products. Palantir has since gone on to become a contractor to all 18 U.S. intelligence agencies and, of course, much more.

At the same time that Peter Thiel was devising the privatization of TIA with his fellow Palantir co-founders, John Poindexter and Alan Wade, he was also suspiciously present in the apparent privatization of yet another DARPA project called LifeLog. LifeLog, at DARPA, was overseen by Poindexter’s close friend Douglas Gage, though it was not housed under the formerly Poindexter-run IAO office as TIA and PAM had been. LifeLog aimed to “build a database tracking a person’s entire existence” that included an individual’s relationships and communications (phone calls, mail, etc.), their media-consumption habits, their purchases, and much more in order to build a digital record of “everything an individual says, sees, or does.” LifeLog would then take this unstructured data and organize it into “discreet episodes” or snapshots while also “mapping out relationships, memories, events and experiences.”

As Unlimited Hangout noted in 2021:

The information that LifeLog gleaned from an individual’s every interaction with technology would be combined with information obtained from a GPS transmitter that tracked and documented the person’s location, audio-visual sensors that recorded what the person saw and said, as well as biomedical monitors that gauged the person’s health. […]

Critics in mainstream media outlets and elsewhere were quick to point out that the program would inevitably be used to build profiles on dissidents as well as suspected terrorists. Combined with TIA’s surveillance of individuals at multiple levels, LifeLog went farther by “adding physical information (like how we feel) and media data (like what we read) to this transactional data.” One critic, Lee Tien of the Electronic Frontier Foundation, warned at the time that the programs that DARPA was pursuing, including LifeLog,“have obvious, easy paths to Homeland Security deployments.”

At the time, DARPA publicly insisted that LifeLog and TIA were not connected, despite their obvious parallels, and that LifeLog would not be used for “clandestine surveillance.” However, DARPA’s own documentation on LifeLog noted that the project “will be able . . . to infer the user’s routines, habits and relationships with other people, organizations, places and objects, and to exploit these patterns to ease its task,” which acknowledged its potential use as a tool of mass surveillance.

The cloud of scandal that had enshrouded TIA and PAM soon came for LifeLog. For instance, Steven Aftergood of the Federation of American Scientists told Wired at the time that “LifeLog has the potential to become something like ‘TIA cubed.’”

Unlimited Hangout’s reporting on the topic continued as follows:

The firestorm of criticism of LifeLog took its program manager, Doug Gage, by surprise, and Gage has continued to assert that the program’s critics “completely mischaracterized” the goals and ambitions of the project. Despite Gage’s protests and those of LifeLog’s would-be researchers and other supporters, the project was publicly nixed on February 4, 2004. DARPA never provided an explanation for its quiet move to shutter LifeLog, with a spokesperson stating only that it was related to “a change in priorities” for the agency. On DARPA director Tony Tether’s decision to kill LifeLog, Gage later told VICE, “I think he had been burnt so badly with TIA that he didn’t want to deal with any further controversy with LifeLog. The death of LifeLog was collateral damage tied to the death of TIA.”

Fortuitously for those supporting the goals and ambitions of LifeLog, a company that turned out to be its private-sector analogue was born on the same day that LifeLog’s cancellation was announced. On February 4, 2004, what is now the world’s largest social network, Facebook, launched its website and quickly rose to the top of the social media roost, leaving other social media companies of the era in the dust.

Perhaps unsurprisingly, the main reason why Facebook was able to so quickly rise to “the top of the social media roost” was thanks to the early involvement of Peter Thiel and his close associates in the company. As noted recently, Thiel had been working to privatize TIA as Palantir with his co-founders as well as John Poindexter, Doug Gage’s close personal friend, the very same year he became involved with Facebook.

Unlimited Hangout’s previous reporting on Facebook’s origins revealed that Thiel, as well as Facebook’s first president –– Thiel associate Sean Parker, were critical to Facebook’s commercial success. Facebook’s success, in turn, has also proven critical to the success of Palantir:

A few months into Facebook’s launch, in June 2004, Facebook cofounders Mark Zuckerberg and Dustin Moskovitz brought Sean Parker onto Facebook’s executive team. Parker, previously known for cofounding Napster, later connected Facebook with its first outside investor, Peter Thiel. As discussed, Thiel, at that time, in coordination with the CIA, was actively trying to resurrect controversial DARPA programs that had been dismantled the previous year. Notably, Sean Parker, who became Facebook’s first president, also had a history with the CIA, which recruited him at the age of sixteen soon after he had been busted by the FBI for hacking corporate and military databases. Thanks to Parker, in September 2004, Thiel formally acquired $500,000 worth of Facebook shares and was added to its board. Parker maintained close ties to Facebook as well as to Thiel, with Parker being hired as a managing partner of Thiel’s Founders Fund in 2006.

Thiel and Facebook cofounder Moskovitz became involved outside of the social network long after Facebook’s rise to prominence, with Thiel’s Founders Fund becoming a significant investor in Moskovitz’s company Asana in 2012. Thiel’s longstanding symbiotic relationship with Facebook cofounders extends to his company Palantir, as the data that Facebook users make public invariably winds up in Palantir’s databases and helps drive the surveillance engine Palantir runs for a handful of US police departments, the military, and the intelligence community. In the case of the Facebook–Cambridge Analytica data scandal, Palantir was also involved in utilizing Facebook data to benefit the 2016 Donald Trump presidential campaign.

Facebook has also proven extremely beneficial to another Thiel and national security state-linked company, the facial recognition firm Clearview AI, whose facial recognition database was largely compiled by scrapping images off of the social media platform.

Given Thiel’s intimate involvement in resurrecting controversial DARPA surveillance programs from the early 2000s, i.e. TIA and LifeLog, it is important to note that Thiel and his network were also intimately involved in the creation and success of two later efforts to resurrect the Policy Analysis Market –– the prediction market platform Augur and, more recently, the prediction market company Polymarket.

Enter Shayne Coplan

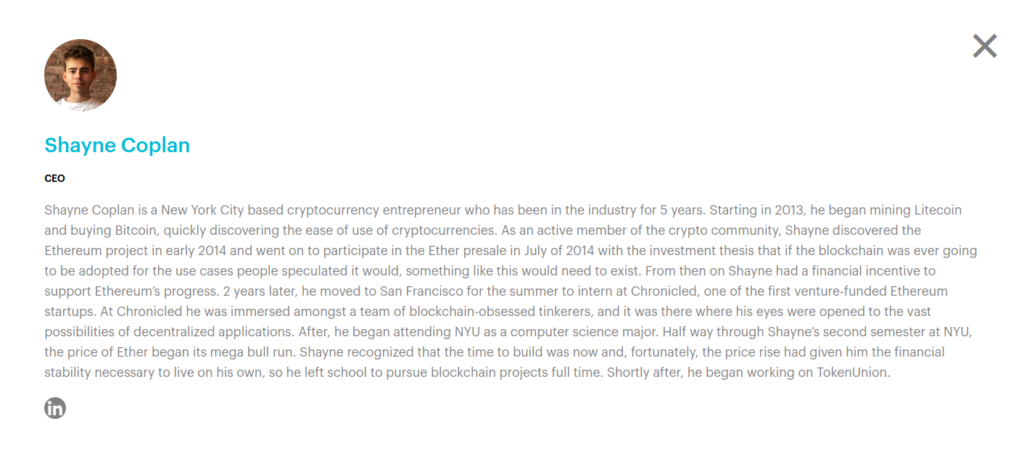

Shayne Coplan, the eventual founder of Polymarket, was raised in New York City, the only child of two South African college professors. He was raised, however, solely by his mother, with Shayne later describing his father as a “mad scientist” who studied panic disorders. Growing up middle class, Coplan developed a “major itch” at a young age to make money, which reportedly drove his early interest in file-sharing websites as well as, later, the nascent cryptocurrency industry.

As he developed this “itch” to aggressively pursue wealth, Coplan simultaneously developed an obsession with the background and early rise of early 2000s tech entrepreneurs who went on to be billionaires, specifically Facebook’s Mark Zuckerberg. Coplan was smart, yet unmotivated and felt like he didn’t stand out enough to compete alongside his peers by conventional means. He would later tell New York Magazine: “I think having a background that was so uncredentialed, it was very clear to me I was a goner if I was gonna go the path everyone else was going and just try and compete there.” Coplan ultimately determined that he would have to emulate his role models much more closely if he truly wanted to follow their example and reap the rewards.

This mindset soon pushed a 16-year-old Coplan to pursue an internship at “what was then one of the city’s hottest startups,” Genius –– a lyric and web-annotation company originally known as Rap Genius. Coplan had repeatedly attempted to contact Genius’ co-founders, who ignored his emails. This led him to travel straight to Genius’ offices where he successfully pitched himself to the people actually running the company. Christopher Glazek, then-executive editor of Genius, later wrote that: “Within minutes [of meeting him,] I learned that Shayne possessed near-encyclopedic knowledge of major tech entrepreneurs, and he eagerly volunteered to add annotations to the Wikipedia pages of Mark Zuckerberg [Facebook] and Travis Kalanick [Uber].”

During the course of his Genius internship, Coplan became “the site’s top expert on the Facebook founder.” Notably, Genius was a 2011 Y Combinator company. That same year saw Yuri Milner and Ron Conway’s SV Angel become intimately involved with the startup incubator. Milner was an important early investor and advisor to Facebook. Conway’s significant connections to the people behind Facebook are discussed later in this article. 2011 was also the year that Sam Altman, widely recognized as a Peter Thiel protégé, became a partner at Y Combinator. Altman would later take over the leadership of the incubator in 2014.

In 2014, Shayne Coplan discovered Ethereum and participated in its initial coin offering (ICO) that same year. He subsequently developed “a financial incentive to support Ethereum’s progress.”A since-deleted biography of Coplan states that Coplan moved to San Francisco some time in 2016 to intern at Chronicled, which Coplan described as “one of the first venture-funded Ethereum startups.” There, he says, he was “immersed amongst a team of blockchain-obsessed tinkerers, and it was there where his eyes were opened to the vast possibilities of decentralized applications.” According to past press releases, one of Chronicled’s goals as a company included “creating a world in which physical and digital experiences are fully synchronized by offering a turnkey solution to securely register any asset identity, from art to automobiles to drones to secure shipping containers and pharmaceuticals, to the blockchain.”

One of Chronciled’s main investors at the time was Pantera Capital, whose co-Chief Investment Officer was Joey Krug around the time that Coplan interned at Chronciled. Krug, a Thiel Fellow who had co-founded the Ethereum-based prediction market Augur, would subsequently join Thiel’s Founders Fund. There, he would become a crucial early investor in Polymarket. Krug, Augur and their significance to this story are explored later in this article.

Armed with glowing recommendations from his former superiors at both Genius and Chronicled, Coplan was admitted to NYU to study computer science and began attending in 2016. However, he quickly became bored and disillusioned. He eventually dropped out halfway through his second semester to “pursue blockchain projects full time.”

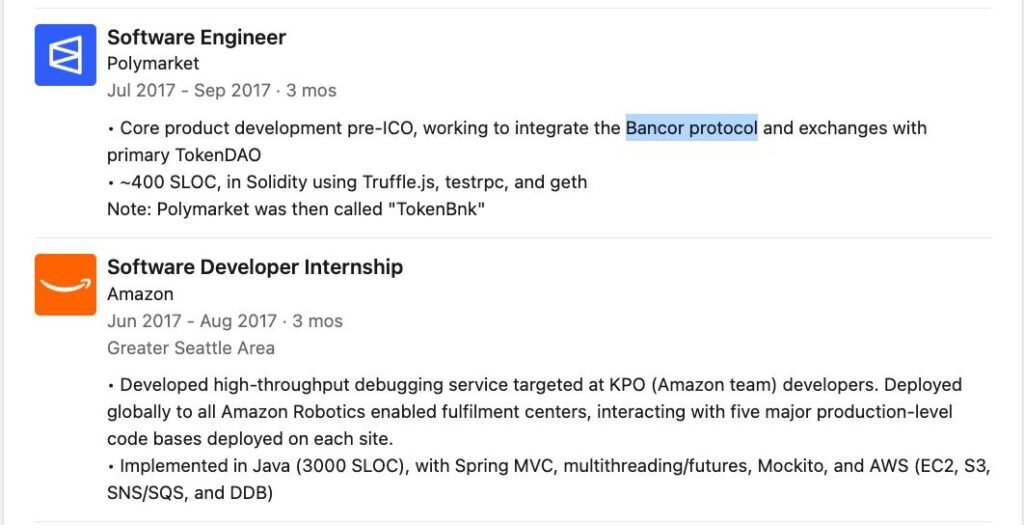

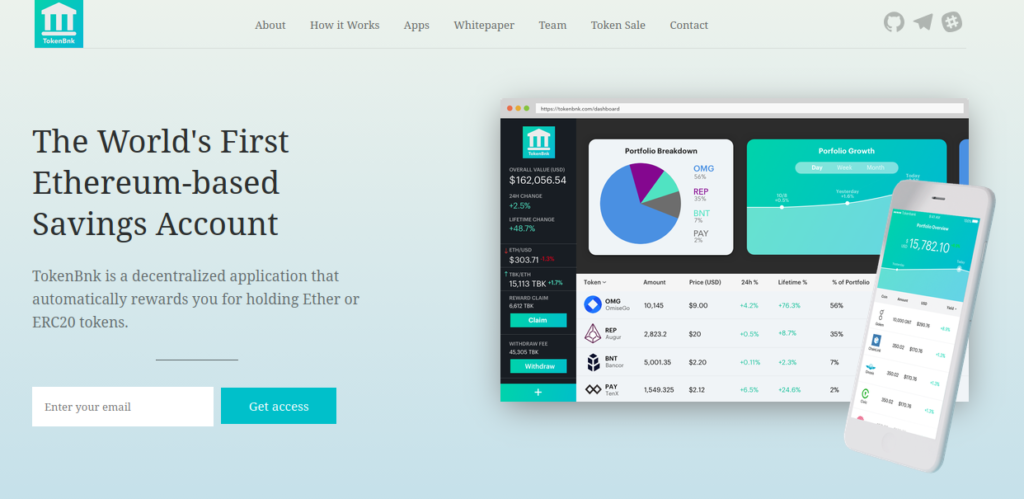

Shortly thereafter, in 2017, Coplan subsequently created a company called TokenUnion, which offered rewards for holding either Ethereum or ERC20 tokens. It initially framed itself as “the world’s first Etherum-based savings account.” TokenUnion was originally founded as TokenBnk and one of its former employees, Yash Patel, has claimed that this company was the direct predecessor of Polymarket. Notably, one of the domains used by TokenBnk/TokenUnion –– tokenunion.io –– now redirects to union.market, another Coplan domain. The shift in TokenUnion domains over the years –– from tokenbnk.com to tokenunion.io to union.market and finally to poly.market and polymarket.com –– seems to suggest that Patel was right. Lending further support to this theory is the fact that all of those domains now redirect to Polymarket.

Oddly, any discussion of TokenUnion is absent from essentially every media profile of Coplan that has been written since Polymarket achieved breakout success a few years ago. All of those media profiles paint Coplan’s success as derivative of pure luck and assure the reader that Polymarket began in 2020 with no real predecessor. In one of those recent media profiles, Coplan asserted he had picked the union.market because of a New York eatery he enjoyed at the time. Though he acknowledges union.market was focused on yield-bearing digital assets, neither he nor the article make any mention of his company TokenUnion. This is despite that the relationship, documented above, between the tokenunion.io and union.market domains. One must wonder why TokenUnion has seemingly been ripped out of the narrative, not just by the mainstream media stenographers chronicling Coplan’s and Polymarket’s rise, but also by Coplan himself.

One of the reasons that TokenUnion has seemingly been erased from current narratives about both Coplan and Polymarket may lie in the TokenUnion’s close partnership and integration with Bancor. Bancor was created by Guy and Galia Benartzi, the nephew and niece of long-time and current Israeli Prime Minister Benjamin Netanyahu. Galia Benartzi, immediately prior to creating Bancor, had been a partner at Peter Thiel’s Founders Fund, where she helped lead the firm’s investments in Israel. One of the main tokens showcased in TokenUnion’s promotional material is Bancor’s BNT token and Bancor is listed among its small list of official partners. TokenUnion’s whitepaper also touted its “integration” with Bancor as one of its platform’s main advantages.

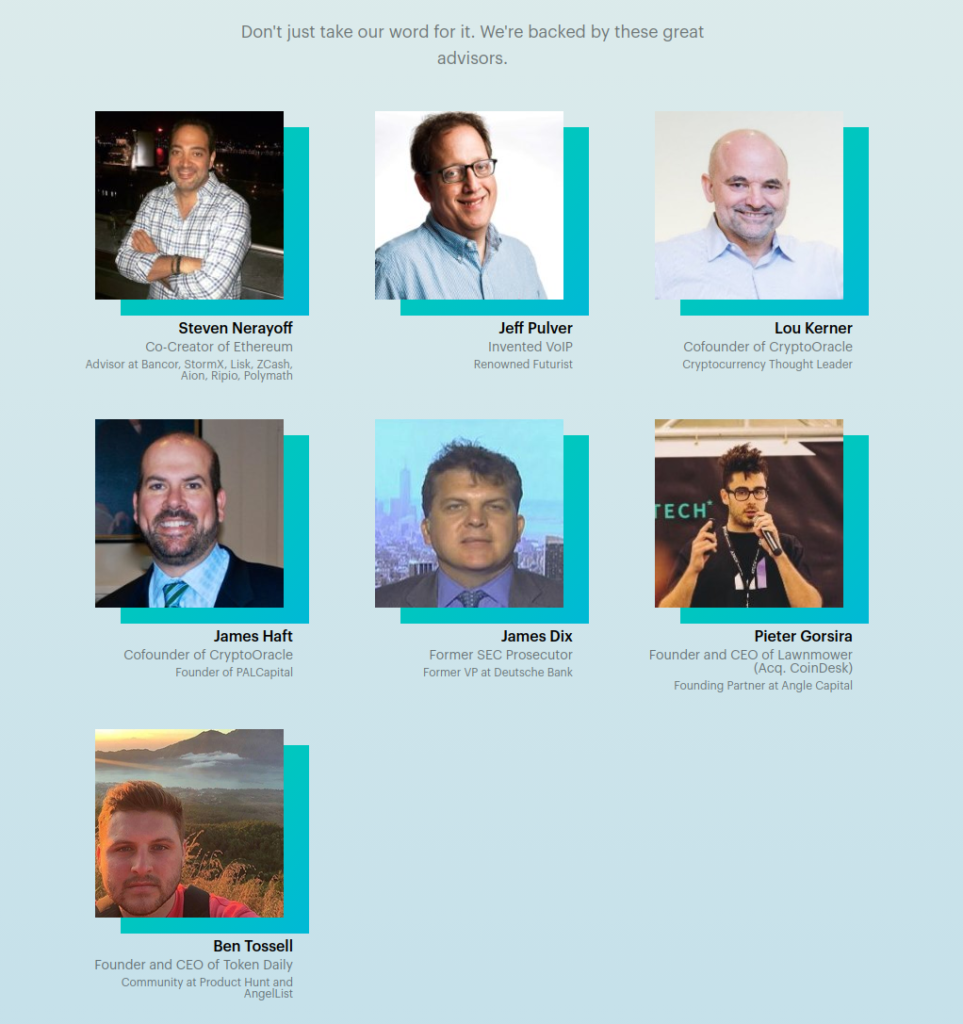

Bancor advisor Lou Kerner was also a TokenUnion advisor, alongside Jim Haft, with whom Kerner created CryptoOracle. CryptoOracle was founded in 2017 and, at the time its founders advised Coplan’s TokenUnion, it focused on supporting “early-stage blockchain firms.” This strongly suggests that CryptoOracle had backed Coplan’s company, which later claimed to have “raised millions in a private presale” from undisclosed sources. Like Bancor, CryptoOracle is also listed as a TokenUnion partner.

Kerner has major connections to the Israeli tech start-up scene, which even former Mossad directors have noted is stuffed with Israeli intelligence veterans and which –– per official Israeli policy –– is full of Israeli intelligence fronts posing as private companies in order to execute projects that were previously performed “in-house” by the Israeli intelligence apparatus. Kerner, who boasts close ties to AIPAC, previously led the Israel Founders Syndicate and is a current advisor of the Israeli Blockchain Association. Kerner is also partnered in an Israeli tech incubator alongside Glilot Capital. Glilot Capital was created by two Israeli military intelligence veterans who invest specifically in “entrepreneurs who emerge from the elite Unit 8200” signals intelligence unit, often likened to Israel’s equivalent of the NSA.

Kerner is notably also a renowned expert on Facebook, not unlike Coplan himself, and claims to have once been offered a quarter of Facebook’s shares by an unknown (but clearly major) Facebook shareholder. He has since declined to specify the extent of his Facebook holdings. Kerner has claimed to have unsuccessfully pitched Mark Zuckerberg to sell him a significant stake in Facebook while Zuckerberg was still a student at Harvard. This suggests that another very early investor or figure at Facebook aside from Zuckerberg (e.g. Sean Parker, Reid Hoffman, Peter Thiel, etc.) had tipped Kerner off to the social media company very early on. Since then, Kerner has also become an investor in Palantir, the privatized TIA that is chaired and was co-founded by Peter Thiel. Kerner previously worked at Bill Gross’ Idealab, the first institutional investor in the Thiel-founded company PayPal. In addition to Kerner, CryptoOracle’s other co-founder Jim Haft as well as another CryptoOracle employee, Jim Dix, are also listed as TokenUnion advisors. Dix is notably listed as a former SEC prosecutor and was previously a vice president at Deutsche Bank.

Notably, Kerner is not the only Bancor advisor who was also an advisor to Coplan’s TokenUnion. Steve Nerayoff, considered the legal architect of Ethereum’s 2014 ICO, was simultaneously an advisor to Bancor and to TokenUnion. An archived version of TokenUnion’s website refers to Nerayoff as the “co-creator” of Ethereum.

Prior to Ethereum’s ICO, the Ethereum white paper, published by Vitalik Buterin in 2014, made note of an alternative consensus mechanism to Proof of Work (PoW) –– which had been popularized by Bitcoin and Ethereum 1.0. This alternative consensus mechanism was called Proof of Stake (PoS).

Proof of Stake removes the “mining” of digital assets via large amounts of compute of specific hashing algorithms and instead creates a randomized lottery system that selects validators based on the weight of shares held in the system –– in this case, how much ETH one holds in a staking contract. Instead of PoW rewarding a Bitcoin miner with transaction fees for “finding” the next block of transactions based purely on how many hashes they can compute, PoS rewards ETH validators with transaction fees in the form of more ETH, the amount of which is based on how many ETH you already own. While the mechanics are novel in their own right, the reality of such a system is that large capital allocators within the ETH system have a larger stake on consensus simply for holding the asset, in addition to generating yield on their stash of tokens simply for holding them.

Prior to the Fall 2022 transition to PoS, termed “The Merge,” the Ethereum Foundation worked closely with stealth start up and Palantir-subcontractor Antithesis to test the new consensus mechanism. In addition, one of the main forces behind the Ethereum blockchain’s move to PoS was Ethereum co-founder Vitalik Buterin, who had been promoting PoS since at least 2017. Buterin is also a Thiel fellow who was closely connected to the founding and development of the Ethereum-based prediction market platform Augur, which was co-founded by another Thiel fellow, Joey Krug.

However, long before Ethereum allowed token holders to earn yield on their ETH stacks via PoS, projects like Bancor and Coplan’s TokenUnion allowed token holders to earn ETH for simply holding ERC-20 (i.e. ETH-based) tokens –– such as the Augur token REP. Augur’s REP and Bancor’s BNT were both advertised on TokenUnion’s website.

In addition, as CEO of TokenUnion, Coplan attended and was a featured speaker at high-profile blockchain and crypto-related conferences alongside executives at major firms like Meta, Microsoft, R3, Visa, Pantera Capital and so on. At the World Blockchain Forum conference in November 2018, Coplan’s speech was titled “the Napsterization of Finance.”

Some time between 2018 and 2019, Coplan contacted Augur’s co-founder Joey Krug, both to complain about Augur’s interface and to pitch him on investments. Krug “made up a random target volume of $5 million a week and told Coplan he would invest if he reached it” with his proposed prediction market venture.

Around this same time, in 2019, Coplan also reached out to none other than Robin Hanson, the system architect of DARPA’s PAM. Coplan, that year, claims to have first stumbled upon a Hanson paper entitled “Shall We Vote on Values, But Bet on Beliefs?” That Hanson paper being the most inspirational to Coplan is notable as it is the paper where Hanson proposes a system of governance based on prediction markets, called futarchy. After reading this paper, per New York Magazine, Coplan proclaimed to Hanson “in a verbose email with multiple block paragraphs that he wanted ‘to be the person to bring prediction markets to life.’” Hanson, who was also advising Joey Krug’s Augur at the time, is said to have largely “brushed off” Coplan.

Coplan went on to “officially” create Polymarket in June 2020, reportedly due to the Covid-19 crisis forcing him to alter course for his previous project “Union Market” and Coplan having recently been inspired by the work of both Hanson and Austrian economist Friedrich Hayek. As the story goes, Coplan then went on by himself and built Polymarket alone “in his bathroom.”

However, that is the official narrative we have been told of Coplan and his early interactions with figures like Krug and Hanson. As demonstrated thus far in this article, another key part of this official narrative around Coplan and Polymarket is a lie. Coplan did not come out of nowhere with Polymarket in 2020 with no real prior footprint or industry connections. Coplan, well before 2020, was speaking at high-profile conferences alongside top executives at some of the biggest companies in the industry while also attracting, per TokenUnion’s own claims, millions in private funding and advisers and partners with clear and obvious ties to both the private and public sector of Israel and significant ties to top people in the early Ethereum network.

In order to paint Coplan’s success with Polymarket as an anomaly and manufacture the appearance of “luck,” TokenUnion has been written out of the narrative. Given this effort to obfuscate Polymarket’s apparent predecessor company, of which Coplan was CEO, one cannot help but wonder what else has been intentionally left out of the story.

Courting the “Thielverse”

Coplan’s aforementioned, years-long obsession with the trajectory of Silicon Valley billionaires, particularly Mark Zuckerberg, is worth dwelling on in detail. During the time that Coplan was a “top expert” on Zuckerberg and prior to officially founding Polymarket, several reports had been circulating about the parallels between DARPA’s LifeLog and Facebook, including the unusual coincidence that Facebook launched the very same day that LifeLog was formally shuttered.

It’s not clear if Coplan knew of such claims or not, but his apparent obsession with Zuckerberg’s –– and Facebook’s –– rise, as well as his professed desire to imitate that trajectory, suggests that he may have been aware of such claims and how they may have factored into Zuckerberg’s professional success. Though, in the event he was not, Coplan surely was aware of the crucial role played by Sean Parker and his associate Peter Thiel in Facebook’s early success and the company’s ability to become the dominant social media company.

If Coplan was to emulate his hero, he surely would need to find his own Sean Parker. However, evidence suggests that Coplan not only sought to emulate Zuckerberg during Polymarket’s formative period, but also Parker as well. As noted earlier, prior to founding Polymarket, Coplan had given a speech at the World Blockchain Forum in 2018 called “The Napsterization of Finance” while serving as the CEO of TokenUnion. Shortly after formally creating Polymarket in 2020, Coplan would claim that Polymarket was at the vanguard of ushering in “the napsterization of finance.”

In order to “napsterize” finance and hold that as a central goal to your business strategy, one must know a considerable amount about the company Napster and what it would mean to “napsterize” an industry. Given that Parker infamously founded Napster after the CIA made efforts to recruit him as a teen, Coplan surely saw both Napster and Parker as models to follow, especially given that Parker was also the first president of Facebook and crucially brought Facebook its first big name investors (e.g. Peter Thiel), thus making him critical to the success of Coplan’s admitted idol, Mark Zuckerberg.

Sean Parker, A Link Between Worlds

Sean Parker was born in 1979 in Fairfax Country, VA to an advertiser and an oceanographer. While plenty has been written about Parker, surprisingly few writers have been explored the interesting, and relevant, background of his father.

Bruce Parker Jr., Sean’s father, spent years working for various government oceanic institutes across the United States, including stints as the chief scientist of the National Ocean Service in NOAA, a director of the Coast Survey Development Laboratory, and a former director of the World Data Center for Oceanography, among others. During his time at the NOAA (from 1974 through October 2004), his department worked closely with the CIA in a data sharing effort spearheaded by Vice President Gore known as Project Medea. Parker’s then-boss at the NOAA, D. James Baker, was a critical part of Project Medea’s team.

Years later, in 2009, Parker Jr. became an active member of the Edge Foundation, founded by John Brockman and largely financed by Jeffrey Epstein. He even penned an introduction for an Edge Special Event! in 2011 titled When We Cannot Predict, in which the first sentence claims that “Prediction is the very essence of science.”

Prior to his time at NOAA, Parker worked directly with the United States Navy, including a summer at the U.S. Naval Underwater Sound Laboratory, and two years supplying the Department of Defense with data as an oceanographer at the U.S. Naval Oceanographic Office. Notably, the NOAA and the Navy have long partnered frequently on “joint ventures” whereby NOAA technology and data are used for both military and civilian objectives (i.e. “dual-use”).

Sean’s grandfather –– water skiing pioneer Bruce Parker Senior –– had his own history with the Navy, helping them train porpoises in the Caribbean. The water ski schools owned and operated by Parker Sr. were partnered with Harry Conover, whose modeling agency was seeded by former U.S. president Gerald Ford and whose wife at the time, Candy Jones, later became the earliest MK-ULTRA whistle-blower years before the Church Committee exposed the CIA project’s existence.

While his father’s lengthy career at the NOAA and the Navy likely saw him brush up against the intelligence community and intelligence assets at times, Sean Parker’s own trajectory would see him interact much more closely with those groups. According to a 2011 Forbes profile on Sean Parker, the FBI raided the 15 year old then-hacker for illegally hacking into websites associated with government services and a Fortune 500 company. He was ultimately let off with community service. During his community service sentence, Parker described meeting a “punk-rock princess” –– with whom he lost his virginity –– as an “incredible cosmic irony.” Parker furthered it was “the most romantic experience of my life,” and that he only met her “because I’d been raided by the FBI.” As the story goes, shortly thereafter, Parker was then recruited by the CIA himself after his success at a local computer science fair.

Parker has claimed that, when presented with the CIA’s offer, he chose instead to work at Mark Pincus’ startup FreeLoader. He later joined the DC-based internet service provider UUNet –– a company that claims to have been the first commercial internet service provider (ISP) that employed many former members of DARPA who had built an early iteration of the internet know as ARPA-NET. Parker’s former boss Mark Pincus later founded the juggernaut Facebook game company Zynga, which at one point accounted for around 10% of the social media giant’s income. Pincus would also come to work with and invest alongside Parker –– including in Polymarket –– after making critical, early investments in several earlier Parker-linked companies, such as Napster and Facebook.

Around the same time Parker began programming at UUNet, Microsoft acquired a 13% in the company. In an August 2011 email to Jes Staley, Jeffrey Epstein implied that Parker –– including his teams at Facebook and Spotify –– were affiliated with “Gates and his entourage.” While Parker should have been in high school, he instead earned “$80,000 his senior year,” and “wasn’t going to school.” According to Parker, “I was technically in a co-op program but in truth was just going to work.” It was during this period that Parker met fellow teenager Shawn Fanning online, and alongside a couple friends, founded the quick-to-fail “internet-security firm” Crosswalk. While not much is available about the firm online today, seemingly, the general concept was that two hackers –– Sean and Shawn –– would share their expertise on breaking into online systems with companies looking to strengthen their cybersecurity.

After his senior year, and with his “co-op program” earnings in hand, Parker put off pursuing college to fly out to San Francisco and co-found the pioneering music-sharing site Napster with Fanning. Parker referred to his time at Napster as “Napster University,” explaining “it was a crash course in intellectual property law, corporate finance, entrepreneurship and law school.” Parker furthered that “some of the e-mails I wrote when I was just a kid who didn’t know what he was doing are apparently in [law school] textbooks.” Despite Napster eventually succumbing to a deluge of high-profile litigation, Parker’s model for disregarding bureaucracy and legislation in the pursuit of technological disruption was established by the young founder’s indifference to the legal context surrounding his company’s services.

Ron Conway, a nearly investor in PayPal and Google, among other stalwarts, met Parker and Fanning at the onset of Napster, and has backed practically every Parker project since. Fanning later referred to Conway as “like family to me,” explaining that he is “such a big part of who I am today.”

However, not every Parker-backed venture was a success, such as the failed start-up Plaxo, which sought to auto-update a person’s email-based address book and was later called a “precursor to social networking.” Parker was infamously forced out of that company in 2004.

Shortly after being kicked out of Plaxo, Parker saw a simply designed website –– “thefacebook.com” –– on the computer owned by his roommate’s girlfriend, who was then attending Stanford. Parker immediately emailed its creator Mark Zuckerberg, much like he had once done with Fanning, and offered to help him with his website.

Matt Cohler, who joined Facebook shortly after Parker, noted the similarity himself: “Napster and Facebook are two of the most significant companies in the history of the Internet and in both cases Parker spotted them earlier than anyone — other than the people who invented them.” By June 2004, Parker had moved into the infamous Facebook villa and became an essential player in the construction of the juggernaut Facebook –– now Meta –– is today.

While Conway decided to initially pass on investing due to concerns with Parker’s then-failing Plaxos contact book company, the second person they called –– early PayPal employee and Pincus’ long-time friend Reid Hoffman –– was too busy founding LinkedIn and instead connected the duo with his former boss Peter Thiel. Thiel quickly invested and joined the board. Joining Thiel and Hoffman was Hoffman’s close friend and Parker’s former boss Mark Pincus.

Forbes later referred to Parker as an early “Facebook’s business veteran” who “helped the college-aged Facebook founders network around Silicon Valley, set up routers and meet benevolent investors like Thiel, Hoffman and Pincus.” Forbes also quotes Zuckerberg as stating that “Sean was pivotal in helping Facebook transform from a college project into a real company,” suggesting that –– without Sean Parker –– Facebook’s enormous success may not have materialized at all.

Parker, Zuckerberg and Thiel went on to change the internet and paved the way for further exploration of the concepts of digital identity, digital content distribution, digital community and even digital currency –– all essential pillars of the now-blossoming prediction market industry. In 2005, Parker was accused of possessing cocaine during a house party at a rental under his name, and although he was never charged, he was essentially forced off of the Facebook board. Despite this, Thiel has claimed that he does not “think Sean ever really left Facebook” and has continued “to be involved in many ways.”

The next year, in 2006, Parker was hired by Thiel and became a partner at Thiel’s Founders Fund. There, he famously courted and advised the team behind Spotify to legally commercialize the digital music industry –– succeeding exactly where Napster “failed.” Thiel reiterated his admiration for Parker, referring to him as “a brilliant entrepreneur who is somehow transforming the United States and yet is not understood by society.”

Not long after, Parker stated that: “It’s technology, not business or government, that’s the real driving force behind large-scale societal shifts.” This idea is similar to those expressed by Parker’s boss Thiel, who has described technology as a way to exert “unilateral change” on the world, and is therefore an “incredible alternative to politics.” Given that Thiel views technology as the most effective way to exert unilateral change on a society and as a way to bypass public consent, his view that Parker, and his companies, have been key to “transforming” the United States takes on increased significance.

One should also consider the early role of Parker and Thiel at Facebook alongside their respective connections to the American National Security State. Parker had early run-ins with the FBI and was sought out by the CIA. As detailed earlier in this piece, Thiel was also actively working to privatize at least some programs of DARPA’s Information Awareness Office at the time Parker contacted him about “thefacebook.com.” Having just privatized DARPA’s TIA program into Palantir, Thiel, and perhaps Parker, certainly saw in Facebook a company that could be molded to serve as more than just a social network. Thiel likely saw its utility as an analogue for the shuttered sister project of TIA, LifeLog, particularly given the fact that Thiel was known to have been meeting with John Poindexter, the close friend of LifeLog’s project manager Douglas Gage, during this time.

Thiel’s fondness for Parker, and his belief that Parker has played a major role in “transforming” the United States, may lie in Parker’s outsized role in developing what we could call the “napsterization” model for a given industry that many Thiel-linked ventures have since followed. Parker’s Napster, even though it failed, was able to test the regulatory environment and determine what was needed for a successor to emerge as a dominant, de facto monopoly in that industry with the blessing of regulators. In the case of Napster’s successor, Spotify, it was Parker –– then at Thiel’s Founders Fund –– who spotted a worthy vessel for his ultimate ambition that began with Napster. Subsequently this “napsterization” model has been applied in several Thiel-linked companies, including Facebook itself via its attempts to launch its Libra stablecoin, as detailed previously by Unlimited Hangout.

For example, Facebook itself faced many legal battles during its formative years, and thus employed many heavy hitters with ties to the public sector as legal counsel, including former State department official Jennifer Newstead, who had previously helped draft the Patriot Act. Another Facebook lawyer, Ted Ullyot, had worked in George W. Bush’s White House before Facebook.

Ullyot himself was suggested to Zuckerberg by Paul Cappuccio, a lawyer who had successfully represented AOL in landmark litigation regarding EU approval –– an outcome that helped globally enshrine American-made interests during the Internet’s proliferation. Both Cappuccio and Ullyot worked at Kirkland & Ellis, the law firm hired to defend Jeffrey Epstein, while Cappuccio helped Parker and Thiel deregulate and disrupt the electronic cigarette market as the general counsel for the now-bankrupt NJOY –– the first eVape company to receive FDA approval.

This “napsterization” model is evident in Coplan’s comments about TokenUnion, which he once referred to as an “economic experiment” that “could ultimately prove to be an integral part and one of the leading methods of storing value in the token ecosystem of tomorrow.” It is certainly interesting that Coplan would be able to attract millions of dollars in seed funding from figures such Lou Kerner and become deeply partnered with Bancor for something that was seen as an “economic experiment” and not a viable, for-profit company. That is, of course, unless the goal of both Coplan and his backers at TokenUnion was economic experimentation with the goal of “napsterizing” major aspects of this industry with a focus on the Ethereum ecosystem. Notably, in a recent media profile, Coplan was asked if he viewed Polymarket as a “technological descendant” of Napster, to which Coplan said “there are parallels.”

While Coplan was building the Ethereum-focused TokenUnion, the Ethereum-based prediction market platform Augur was taking off. Advised by Ethereum co-founder Vitalk Buterin and Robin Hanson and financed in part by a Thiel fellowship, Augur eventually “failed” to succeed in creating a globally successful prediction market. Developed and maintained by the Forecast Foundation non-profit, Augur had hinted–– before it became largely relevant and Krug left the foundation –– that it would offer a “widely anticipated for-profit spin-off.” Shortly after Krug stopped working on Augur, he joined Sean Parker at Thiel’s Founders Fund.

In keeping with the “napsterization” model, Krug and Founders Fund, with lessons learned from Augur, would become early investors and advisors to the for-profit Polymarket. Krug has since commented on the “symmetry” between the evolution of Napster into Spotify, via Sean Parker at Founders Fund, and the evolution of Augur into Polymarket, via Krug’s role at Founders Fund.

Joey Krug: Augur, Ethereum and Market Force Divination

Joey Krug, born in 1995, began mining Bitcoin in his bedroom in May 2011 ––at around 15 years old. By late 2013, Krug was inspired by a recent price surge to pursue cryptocurrency more seriously, and began a bitcoin club at his university, eventually founding a bitcoin point-of-sale company. In 2014, Krug teamed up with his college friend Jeremy Gardner and a computer scientist named Jack Peterson to put together a decentralized prediction market called Augur. Augur was inspired and derived from a Bitcoin-based project called TruthCoin. The first version of the white paper for TruthCoin was published in December 2013 by Paul Sztorc.

Interestingly, only three years before the renewed interest in cryptocurrency-based prediction markets, DARPA’s sister agency — the Intelligence Advanced Research Projects Activity (IARPA), which is responsible for “pay[ing] for experimental projects for the U.S. intelligence community” — announced they were launching “a four-year, $50 million program” that would pay people willing to predict major world events. This program, known as Aggregative Contingent Estimation, or ACE, was headed by Jason Matheny. After running ACE and, later, IARPA as a whole, Matheny launched the Center for Security and Emerging Technology (CSET) with a $55 million grant he received from the Open Philanthropy Project –– co-founded by Facebook co-founder Dustin Moskovitz. The ACE program officially ended in June 2015, shortly after Krug formalized the non-profit entity tied to Augur development –– the Forecast Foundation.

Soon after the launch of the Ethereum network in 2014, Ethereum co-founder Vitalik Buterin approached Krug. Buterin had recently received a Thiel fellowship to further the development of Ethereum. Buterin convinced Krug to develop what would become the prediction market Augur, not on Bitcoin as originally planned, but on Ethereum. Buterin argued that doing so would allow Krug to take advantage of a more expressive smart contract programming language than what was then available on Bitcoin.

Krug and his team, now counting Buterin as an advisor, then founded the Forecast Foundation in Estonia in December 2014 as a non-profit entity meant to further develop the Augur platform. Another advisor, Ron Bernstein, was the co-founder of InTrade, which previously had partnered with DARPA to provide data for their PAM experiments. Bernstein’s Tradesports.com, which had acquired InTrade in 2003, had leased the technology to the Forecast Foundation behind Augur in exchange for REP tokens created during their groundbreaking fundraiser –– leading Tradesports.com to amass a large ETH stake after it converted its REP token holdings into ETH.

Interestingly, during this same time, Augur co-founder Jeremy Gardner posted in 2015 that some on the Augur team were “speaking to a few several-letter agencies” to “help them understand the technology we’re building.” Gardner went so far as to say that “the DoD, DARPA, and CIA are huge fans of Augur” and the prediction market platform it sought to build. Upon leaving Augur in a messy lawsuit, Gardner joined Blockchain Capital –– an influential cryptocurrency venture firm founded by Tether co-founder Brock Pierce, which features prominently in The Chain series.

Notably, the Augur team soon added the architect of DARPA’s failed PAM prediction market, Robin Hanson, as an advisor. The Augur logo notably bears significant similarities to the logos of DARPA’s failed TIA and PAM projects (i.e. a “one-eyed” pyramid). In fact, a profile on Augur from 2018 notes that Krug, one of his co-founders, and two unnamed Augur advisors (one of which was likely Hanson) had explicitly decided to make the Augur logo “a pyramid, with three points converging upon an all-seeing eye.” This, among other similarities, suggests that Augur was an effort to resurrect PAM, particularly given that, in a few short years, Thiel’s tentacles would extend deeply into Augur and were already present, indirectly, via Buterin’s Thiel fellowship.

In the fall of 2015, the Forecast Foundation and Augur operated the first ever initial coin offering (ICO) on the Ethereum blockchain with their token REP. Reports from October 2015, during its ICO, claim that Augur was courting “four major banks,” in addition to a partnership with IBM Watson in efforts to develop a “closed-source alternative” to Augur. This fundraising method, analogous to the initial public offering (IPO), came to dominate the remainder of the decade in the cryptocurrency space –– leading its pioneer Krug to eventually join two of the most influential investing firms in the industry, Pantera Capital and Peter Thiel’s Founders Fund. In June 2016, Krug himself was awarded a Thiel Fellowship to further develop Augur. The next year, he joined Dan Morehead’s Pantera Capital as a co-chief investor officer (CIO) in 2017.

In a June 2017 post published on his Medium announcing his Pantera appointment, Krug specifically noted that this would help solve a dire need for liquidity on Augur, even stating that Pantera would be actively trading on it:

Once Augur is out, we can even trade on it, which will increase liquidity and be good for everyone. There are no set allocations for anything in the fund, it is all about capacity and what we can spend the money on that is the best investment/most profitable.

If a million people show up day one of Augur’s full release, then there is probably no need (or edge) for us to trade. But if it does not happen, we will trade as long as we have an edge. This is not altruism: we are not planning to lose money to attract users to Augur! However, since we have an edge even in markets like bitcoin, we will almost certainly have an edge on Augur markets for quite a while.

In July 2018, Augur released its primordial iteration based upon the native Ethereum network token, ETH, and its REP token that had been created during its groundbreaking ICO. According to Krug, version one of Augur was “a very slow, expensive, difficult to use version” and left users exposed to varying price fluctuations of tokens. As the Augur blog noted in 2021, version one was “the first real world deployment of a free and open prediction market,” which “allowed the community to test many hypotheses and ideas that had been written about for decades prior by many academics, software engineers and free-market information enthusiasts.” In other words, it was an economic experiment.

Version two of Augur, launched in 2020, replaced the unit of account with a stablecoin, specifically using DAI –– an algorithmic stablecoin managed by MakerDAO. Despite version two solving a lot of issues from version one, it “became clear that Augur was too resource-intensive to live fully on Ethereum mainnet.” Due to this and because of the evolution of externally-traded Augur shares on existing automated markets, the Forecast Foundation was “ultimately” led to launch Augur Turbo in 2021. Augur Turbo partnered with oracle provider Chainlink and Ethereum Layer 2 (L2) Polygon –– both infrastructure partners that Polymarket would utilize only a few years later.

These decisions to move towards L2s and stablecoins were anything but trivial. In fact, Krug himself has expressed that, without cryptocurrency, prediction markets would be unable to function. According to Krug, two of the main pillars of the prediction market industry at large –– a 24/7 global, internet-based market and (practically) irreversible transactions –– helped “unlock” prediction markets’ ability to function and succeed.